Every trip to the supermarket lately, I buy roughly the same things — and the total at the register keeps creeping up.

At 10X we run a platform for online supermarkets, and we keep hearing from partners that costs are rising and passing those increases through to shelf prices is hard. I wanted to see how the wave of price hikes in the news actually shows up in store performance and earnings.

The structure of the price-hike wave

Start with scale.

According to Teikoku Databank's survey of price changes at 195 major food companies (June 2026), the number of items slated for price increases in 2026 is on track to exceed 10,000 for the fifth year in a row since the survey began in 2022. The 2025 full-year total was 26,609 items (+64.6% year on year).

The drivers are no longer just raw materials. The same survey (as of June 2026) reports:

- Raw materials: still the largest factor (~98%), but trending down

- Packaging and materials: 73.7% (naphtha-linked materials, Middle East tensions)

- Logistics: 74.1% (highest level within 2026)

- Labor: 54.7%

- Middle East tensions: 22.7% (newly visible)

On top of post-invasion commodity inflation, summer 2026 added packaging, logistics, and energy. Truck-driver overtime rules from the "2024 problem" are still part of the logistics story.

Those costs stack up from manufacturer to wholesaler to store to register — and eventually bounce back as consumer choice about where to shop.

Winners and losers in monthly and annual results

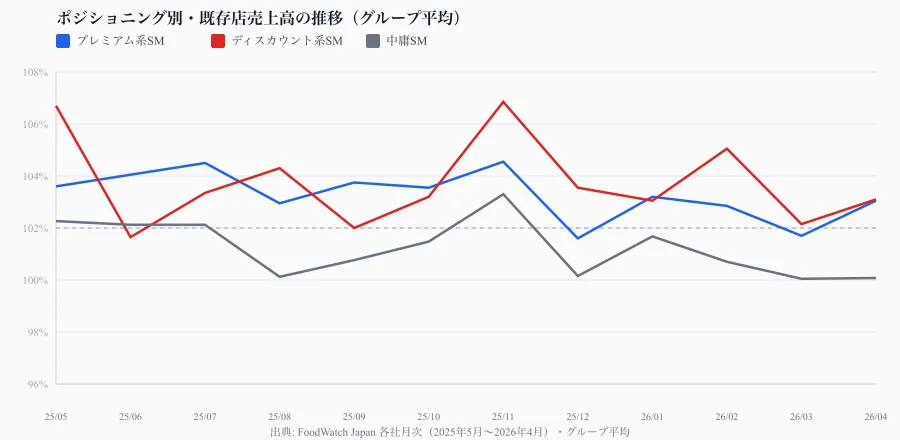

Listed supermarkets disclose same-store sales (year on year) every month. I pulled 12 months of data from May 2025 through April 2026 from FoodWatch Japan (May 2026 is not yet on FoodWatch).

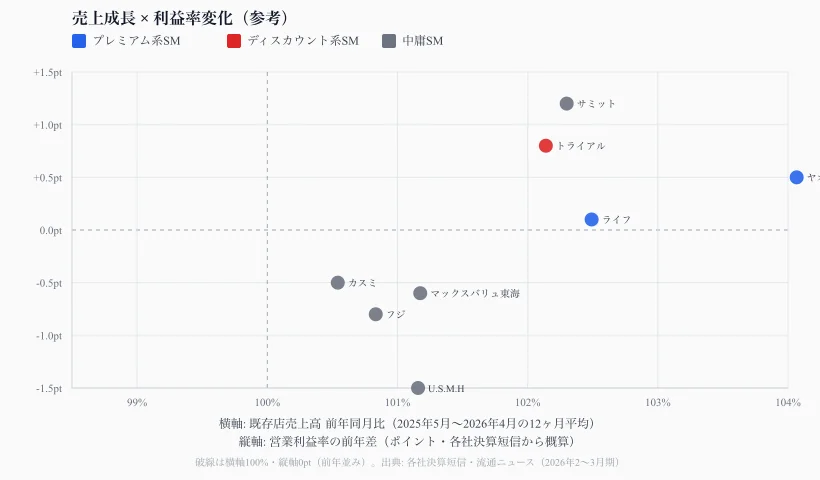

At the earnings level, the split is clear. Ryutsu News' Kanto supermarket ranking (May 2026) shows Life up 2.9% in operating profit (22 straight years of revenue growth) and Summit up 19.4%, while Fuji grew revenue but operating profit fell 13.4%, and U.S.M.H posted a net loss of ¥3.18 billion.

Revenue up, profit flat or down — familiar in inflation. Grouping the monthly data by positioning makes the pattern clearer.

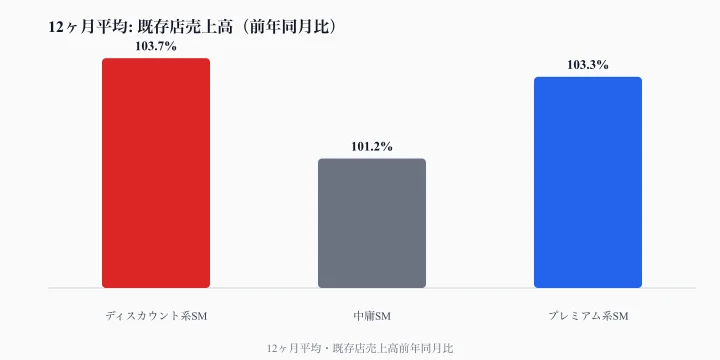

What positioning shows

I grouped chains into three rough buckets and compared 12-month averages of same-store sales.

| Positioning | Examples | 12-month avg. (same-store sales, YoY) |

|---|---|---|

| Discount | Valor, Trial, Mamiya Mart, etc. | 103.7% |

| Strong PB / premium | Life, Yaoko | 103.3% |

| Middle | Maruetsu, Kasumi, Fuji, Aeon SM banners, Izumi, etc. | 101.2% |

Source: FoodWatch Japan monthly data (May 2025–Apr 2026). Simple within-group average; only chains with data in a given month are included. Discount group includes Trial HD monthly (May 2025 and Mar 2026 not disclosed) and Mamiya Mart (Mar–Apr 2026 only, from trade press).

The middle group has hovered around 100% since late 2025 — consistently below both ends.

In Mar–Apr 2026 individually: Life (+1.3%→+2.8%) and Yaoko (+2.1%→+3.3%) and Valor (+4.1%→+3.7%) held up, while Kasumi, Fuji, and Maxvalu Tokai were below prior year. Aeon Food Style (formerly Maxvalu Kanto) was flat; Izumi was relatively stable around +1%.

Dashed lines mark prior-year parity (100% sales, 0pt margin). Vertical axis: approximate YoY change in operating margin (pt) from earnings releases. Illustrative, not a strict like-for-like comparison.

The positioning question, now

Price hikes are structural, not malice. Manufacturers, logistics, and stores each carry different taxes on the way to the shelf.

Consumers are sorting themselves:

- Discount (Lopia, OK, Valor, Trial, Kobe Bussan / Gyomu Super) — "cheapest wins"

- Premium PB (Life, Yaoko) — private label and assortment defend basket size

- Middle — neither "closest and convenient" nor "clearly cheap"

The more you sit in the middle, the easier it is for price promotions to protect traffic at the expense of margin — exactly what U.S.M.H described when gross margin fell despite pricing actions.

From our platform work, partners differ sharply in PB mix, pass-through, and basket growth. Before tools and AI, "why would someone choose us?" may be the heaviest question.

I wrote about the hidden tax platforms pay. This is the retail-side mirror: structural costs and the choice of positioning.

I want local supermarkets to survive

Personally — in Community Ties and Rootlessness I wrote about growing up in rural Aomori where the local supermarket was woven into daily life. Moving to Osaka, I came to value that "smell of the place" again through my kids and neighborhood stores.

Delicia in Nagano, Izumi's food floors in regional shopping centers — they offer something a standard national box cannot.

The data is not a threat; it is material for decisions. Middle positioning without a deliberate choice is getting harder. I still want those stores to remain — and I want the numbers to inform how, not whether, they fight for that.

Comments

Share your thoughts or questions. Comments are published after approval.

Write a comment