This is part 4 of my series on retail. Here I research the Japanese consumer co-op system (生協, pronounced "seikyo") — a massive food infrastructure that's deeply embedded in Japanese society but poorly understood from a business perspective.

Thanks to my friend and 10X angel investor @hik0107, who did the original research with me two years ago.

Almost everyone in Japan knows what a co-op is. You might remember the thick mail-order catalog that appeared at home, where you checked boxes to order items each week. Or perhaps the memory is of a truck arriving at your apartment complex every week, where neighbors would gather to receive their orders together.

Go almost anywhere in Japan — even the most rural areas — and you'll see co-op trucks on the road. I grew up in Aomori, at the very northern tip of Honshu, and they were there too.

But understanding co-ops from a business perspective — their scale, their organizational structure, their infrastructure, their prospects in the digital age — is genuinely difficult. For example, the IGD report "Leading global online grocery markets to create a $227bn growth opportunity by 2023" appears to have miscategorized Japanese co-ops (likely counting their full GMV as online), which shows how hard they are to analyze from the outside.

Co-ops started as consumer mutual aid organizations

Japanese co-ops are different from corporations. They were founded as organizations by consumers, for consumers — members invest their own capital, run the organization themselves, and use it themselves. This fundamental character has persisted to the present.

The core business is purchasing co-ops (supply operations), but many co-op organizations also run mutual aid insurance, medical services, and facilities.

Co-ops are also categorized by origin: regional co-ops, workplace co-ops, and university co-ops are the main types. This article focuses on regional purchasing co-ops — the ones that form the food distribution infrastructure.

A note on data: the line between what statistics cover and don't cover is usually implicit in co-op reporting. Accurate breakdowns are difficult even internally. The figures here should be read as directional.

Purchasing co-ops are Japan's largest food delivery operator

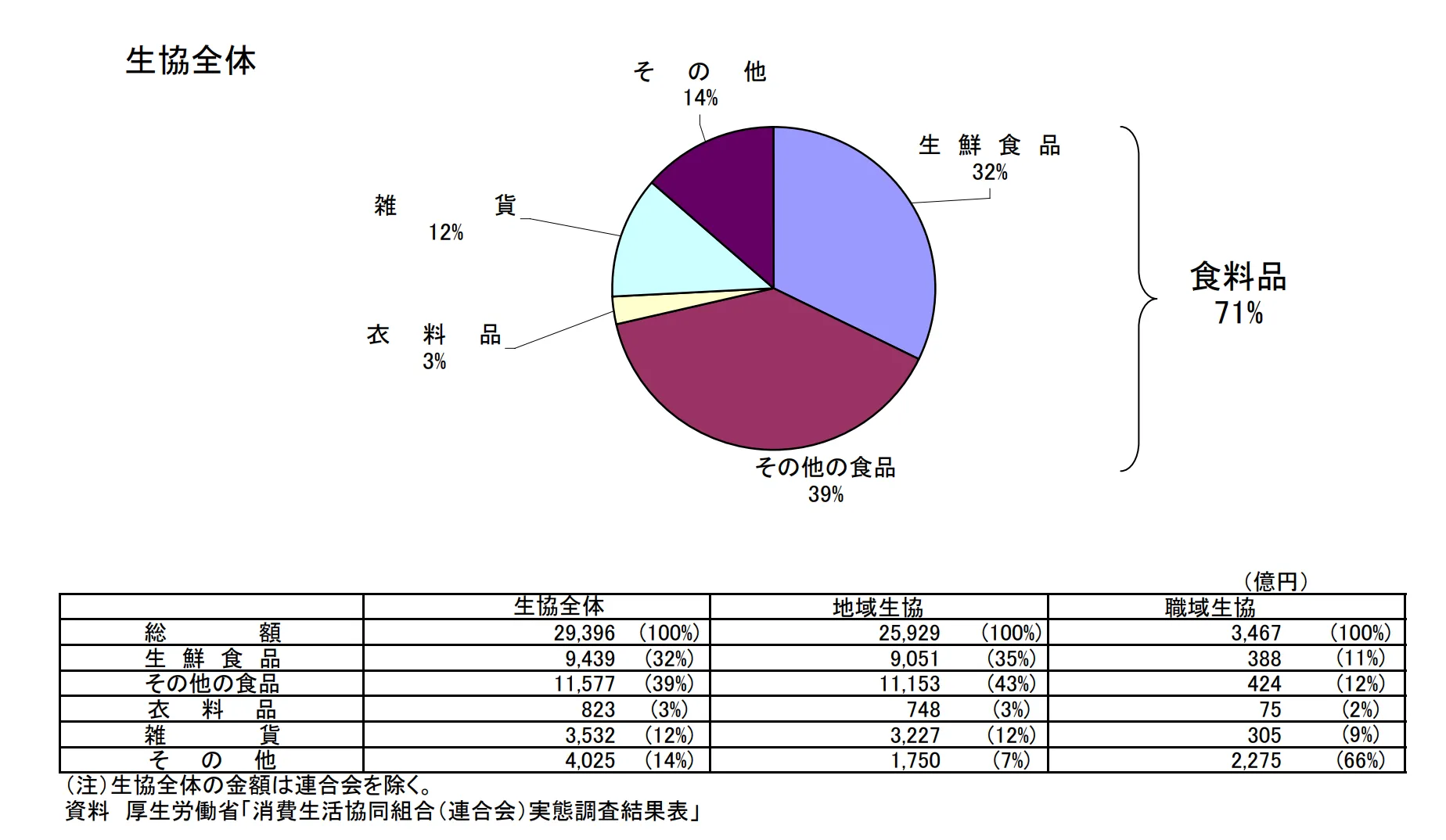

Purchasing co-ops primarily sell food to members. As of 2004, 71% of their business was food.

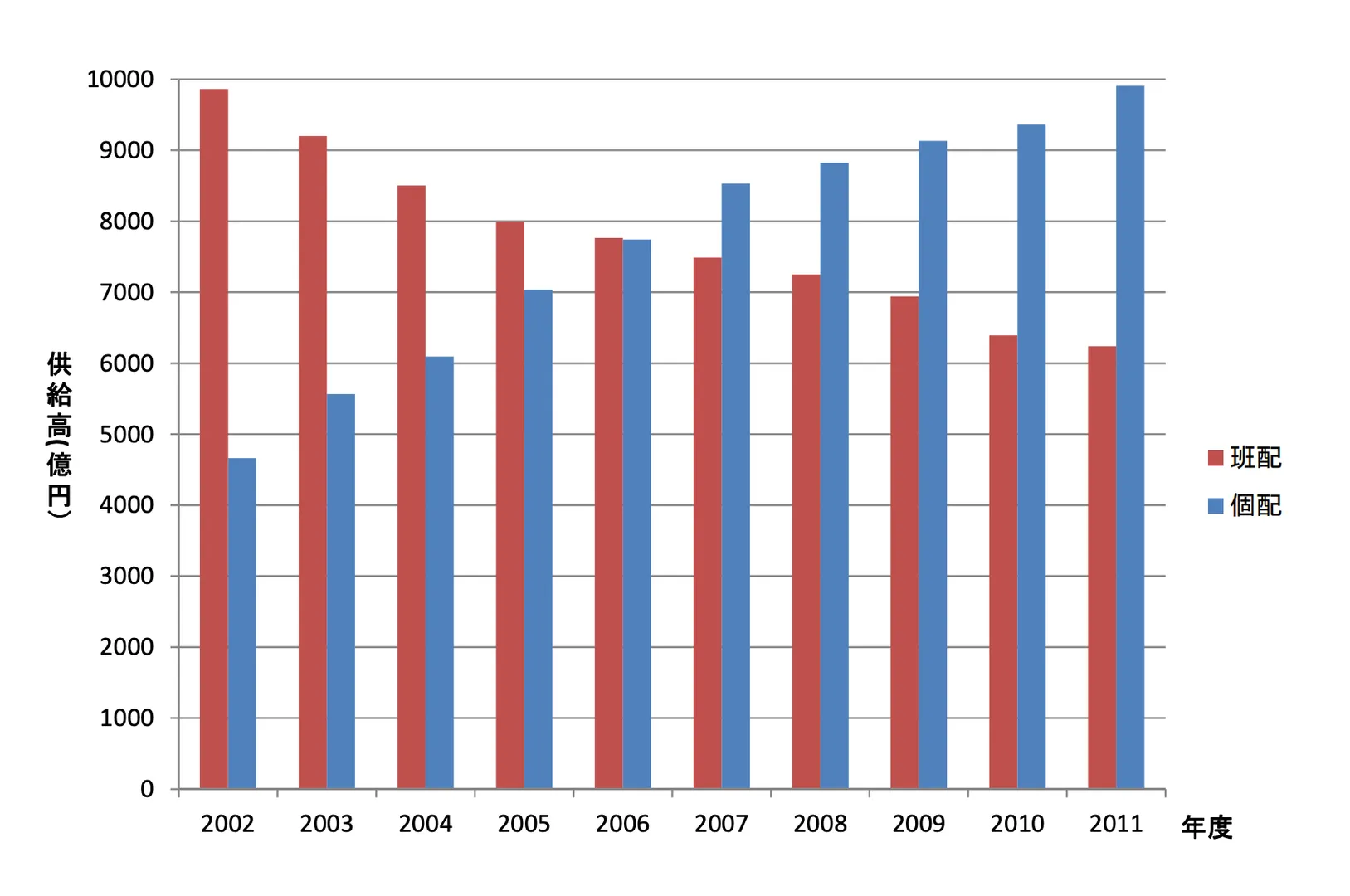

The purchasing business has two segments: in-store retail and home delivery. Home delivery further divides into individual delivery (each household receives directly) and group delivery (a truck delivers to a coordinated stop for multiple households, originally organized around apartment complexes or neighborhood groups).

The group delivery model is fascinating — it was essentially a precursor to social commerce decades before pinduoduo existed. A coordinated group of neighbors placing orders together and receiving them at one point.

The purchasing co-op's annual GMV is ¥2.7 trillion (FY2018) — larger than Aeon Retail's approximately ¥2.2 trillion, making co-ops Japan's largest food retailer by volume.

The breakdown: in-store ¥0.9T, individual delivery ¥1.3T, group delivery ¥0.5T. From 2002–2011, group delivery's share shifted toward individual delivery. "From group to individual" has been the trend.

A complex, decentralized governance structure

Understanding co-op governance is genuinely difficult.

The national body

The closest thing to "co-op headquarters" is the Japanese Consumers' Co-operative Union (JCCU). Its board includes directors from regional co-ops and business federations across Japan.

JCCU has a published org chart that looks similar to a large company's. Its functions include branding, product MD (merchandise development), catalog ordering, and logistics support — essentially operating as headquarters providing operational support to individual co-ops.

Business federations

Below the JCCU are 12 business federations (jigyo rengo), organized either by geographic area or by ideology (the particular social or political tradition the co-op emerged from). Federations coordinate joint activities among member co-ops: product development and procurement, catalog production, and so on.

Regulatory oversight

Co-ops that operate within a single prefecture are overseen by that prefecture. Federations spanning multiple prefectures answer to regional health bureaus or, in some cases, directly to the Minister of Health, Labour and Welfare. This is why MHLW's website contains summary data on co-ops — but also why MHLW doesn't have complete data.

Subsidiaries

Under JCCU are subsidiaries including CO-OP Information Systems (IT) and CX Cargo (logistics). JCCU holds 100% of these companies and uses them to provide EC systems and logistics infrastructure to member federations.

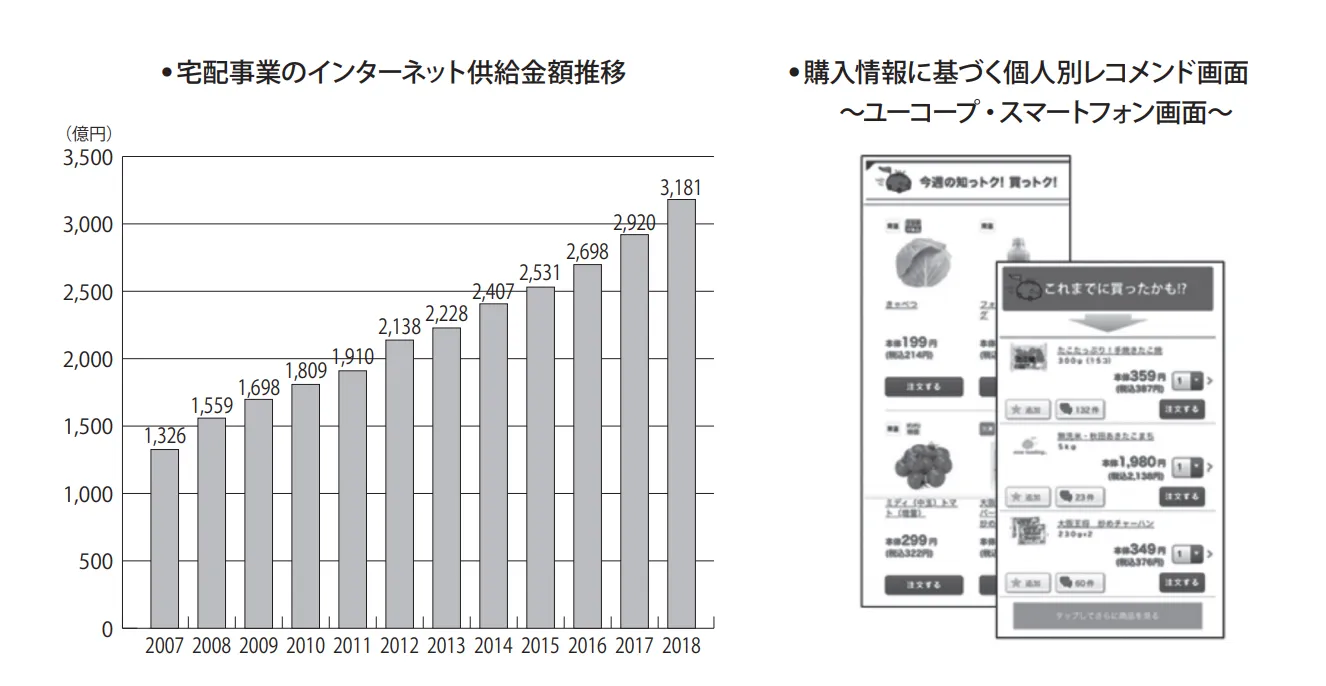

EC status: approximately 17% of home delivery GMV

In FY2018, home delivery GMV was ¥1.8 trillion, of which ¥318.1 billion came through EC — a 17-18% EC rate. Year-on-year growth has been 7-10%, consistent and steady. Against total purchasing GMV of ¥2.7 trillion, EC is roughly 10-12%.

Registered online members number 3.75 million, with 1.18 million average weekly buyers — a remarkably high utilization rate among registrants.

Internet use also supports member acquisition. According to JCCU data, 103 co-ops jointly drove 481,000 resource requests through their "start co-op delivery" website (FY2018, +24% YoY). Online signup processes are also expanding — as of FY2018, 72 co-ops (about 15% of the total) could complete delivery enrollment entirely online.

However, a problem: the systems provided by JCCU are not necessarily being used to solve these challenges. From conversations I had with people at business federations, the centrally provided systems have usability issues. Federations with the capital to do so are building their own apps and web interfaces independently. Fragmentation is accelerating.

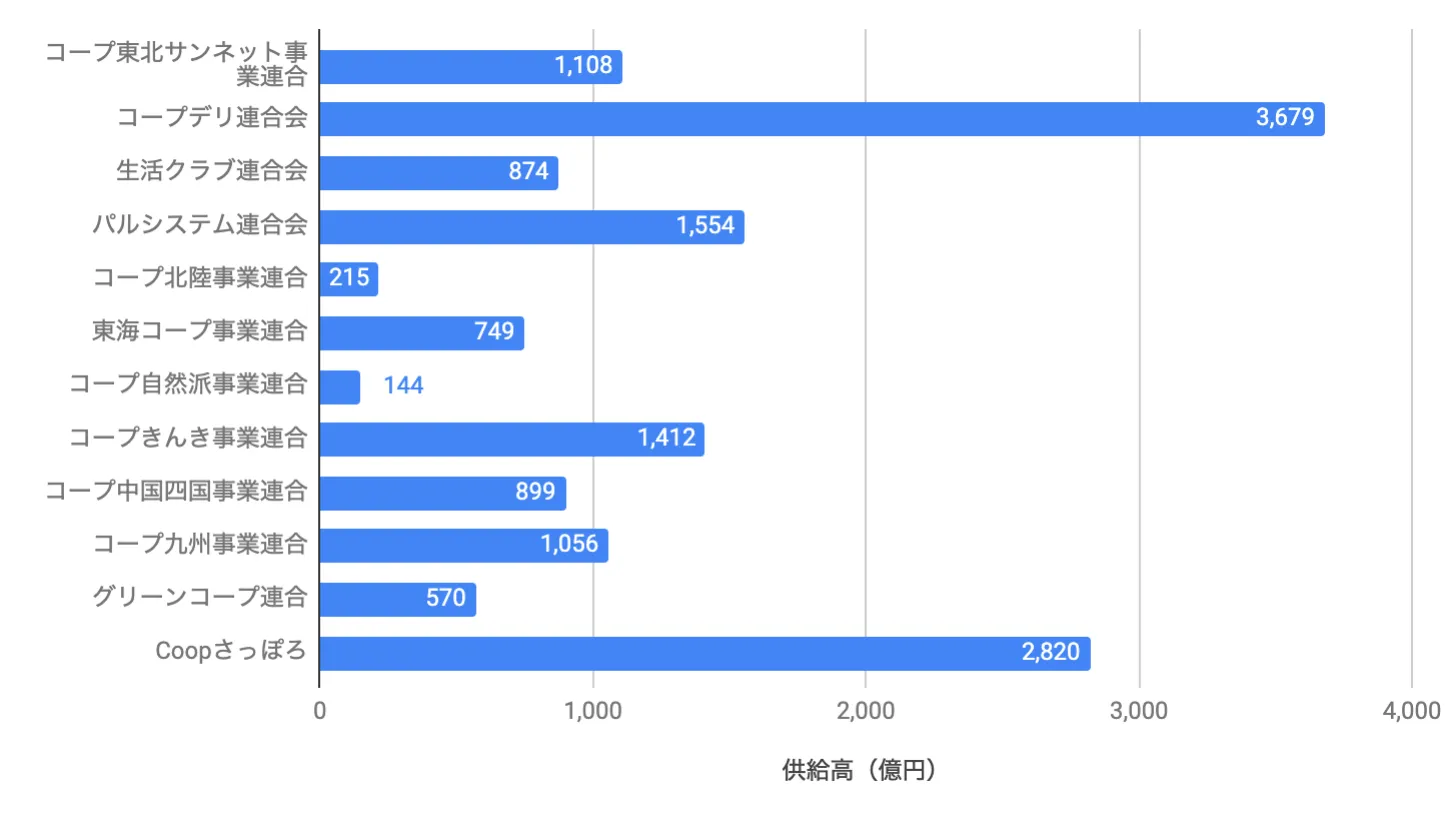

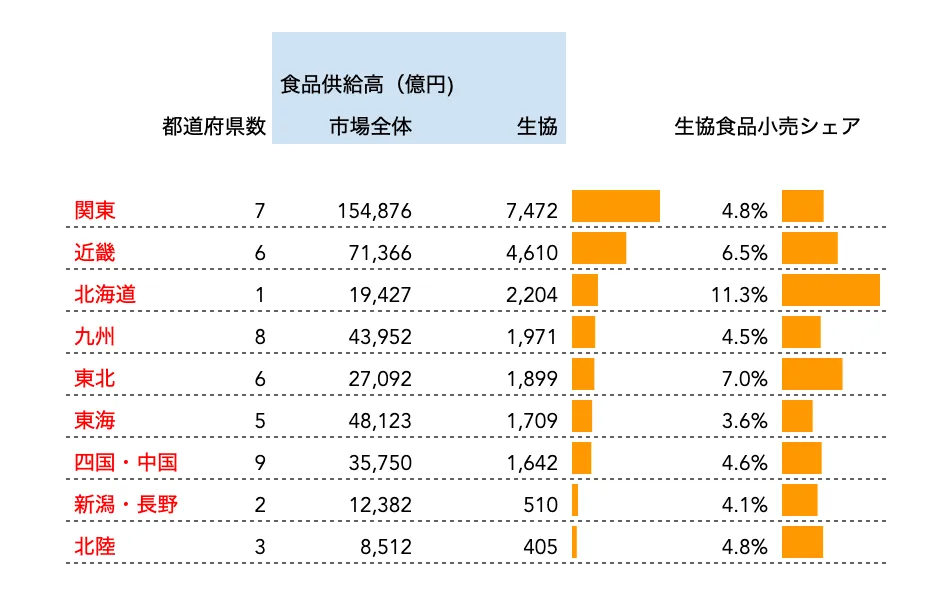

Business federation GMV and regional market share

Below is a comparison of 11 business federations plus Coop Sapporo:

Federations are often competitors within overlapping regions — "the enemy of a federation is another federation" is a real saying.

Coop Sapporo (Hokkaido) deserves special mention: it was formed by consolidating 9 separate local co-ops under strong leadership, and is now the fastest-moving co-op organization in Japan, uniquely covering an entire region.

Regional food retail market shares:

In Hokkaido, Coop Sapporo alone holds 11% of the food retail market. In the Tokai region (around Nagoya), co-op share is only 3.6%. The difference across regions is roughly 3x.

How are other catalog mail-order businesses handling the digital transition?

Co-ops are best understood as catalog mail-order businesses: members select from a paper catalog, place orders, and receive delivery a week later. So how are other catalog mail-order businesses navigating the EC transition?

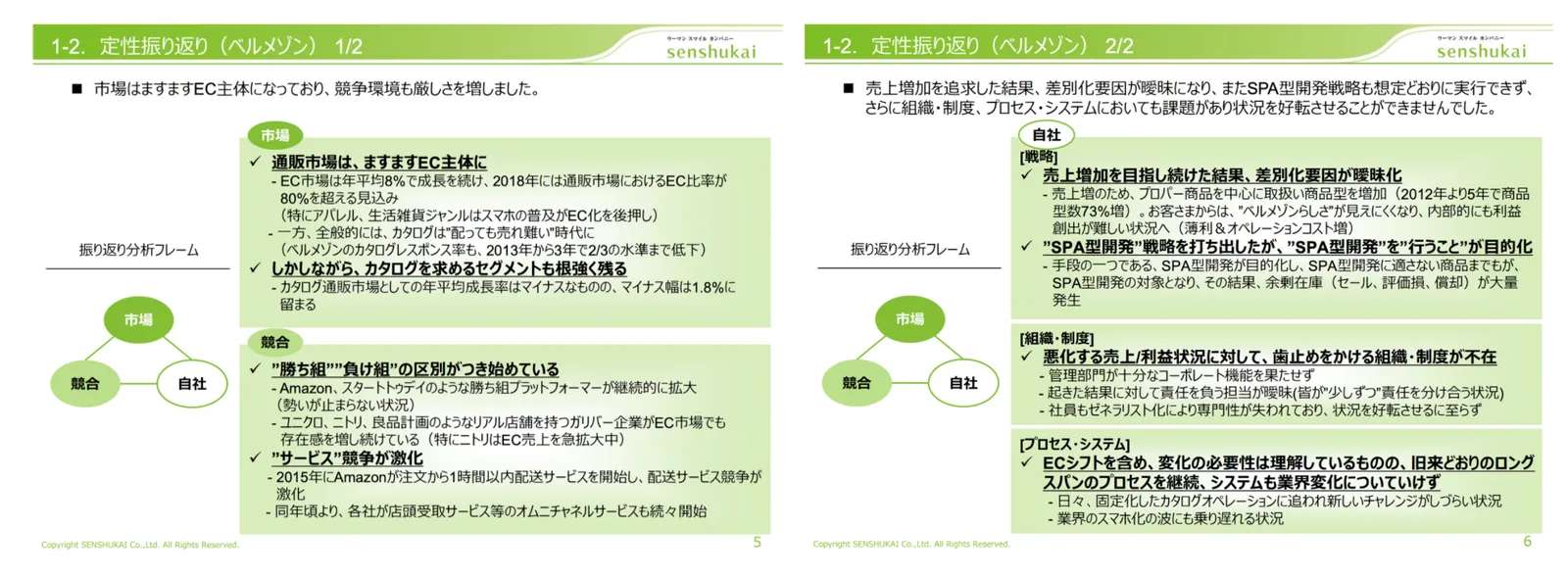

The short answer: with difficulty, but with emerging new direction. Let me look at Senshukai (Belle Maison), one of Japan's major general mail-order companies.

Senshukai positioned itself as a "Women Smile Company" — a relatively focused women's apparel catalog business. It was successful at retaining its core customers, but overall company performance has struggled.

They built their own EC platform and EC rates rose — but the EC channel was mostly used as an "ordering terminal": customers browsed the paper catalog and typed in product codes online. Product development cycles and speeds didn't shift to EC-native rhythms (slow, dependent on catalog publication schedules). They couldn't match the product development speed of pure-play EC businesses.

Their 2017 medium-term plan explicitly acknowledged the tough environment and called for an EC shift:

Looking at their 2019 full-year results: the answer they landed on was shifting from proprietary EC to accelerating their presence on Rakuten and Amazon. In other words: outsource platform building, operation, and customer acquisition to specialists, and focus the company on inventory operations and branding. By abandoning the pursuit of top-line growth for its own sake, they recovered profitability.

This 2017 article captures the sense of crisis that led to this decision:

- Willingness to accept revenue decline in exchange for the biggest catalog volume reduction in company history

- Recognition that the catalog business model — fixing product plans a year in advance, carrying inventory, selling on catalog timing — had an uncertain future

- Despite breaking 80% of orders coming through the web for the first time, admission that the catalog-dependent culture hadn't broken free, and the need to shift to "net-native business flows" as fast as possible

What's next for co-ops?

Compared to apparel catalog businesses like Belle Maison, co-ops face much less external competitive pressure. But trends are emerging: an aging customer base, and younger demographics gravitating toward online supermarkets instead.

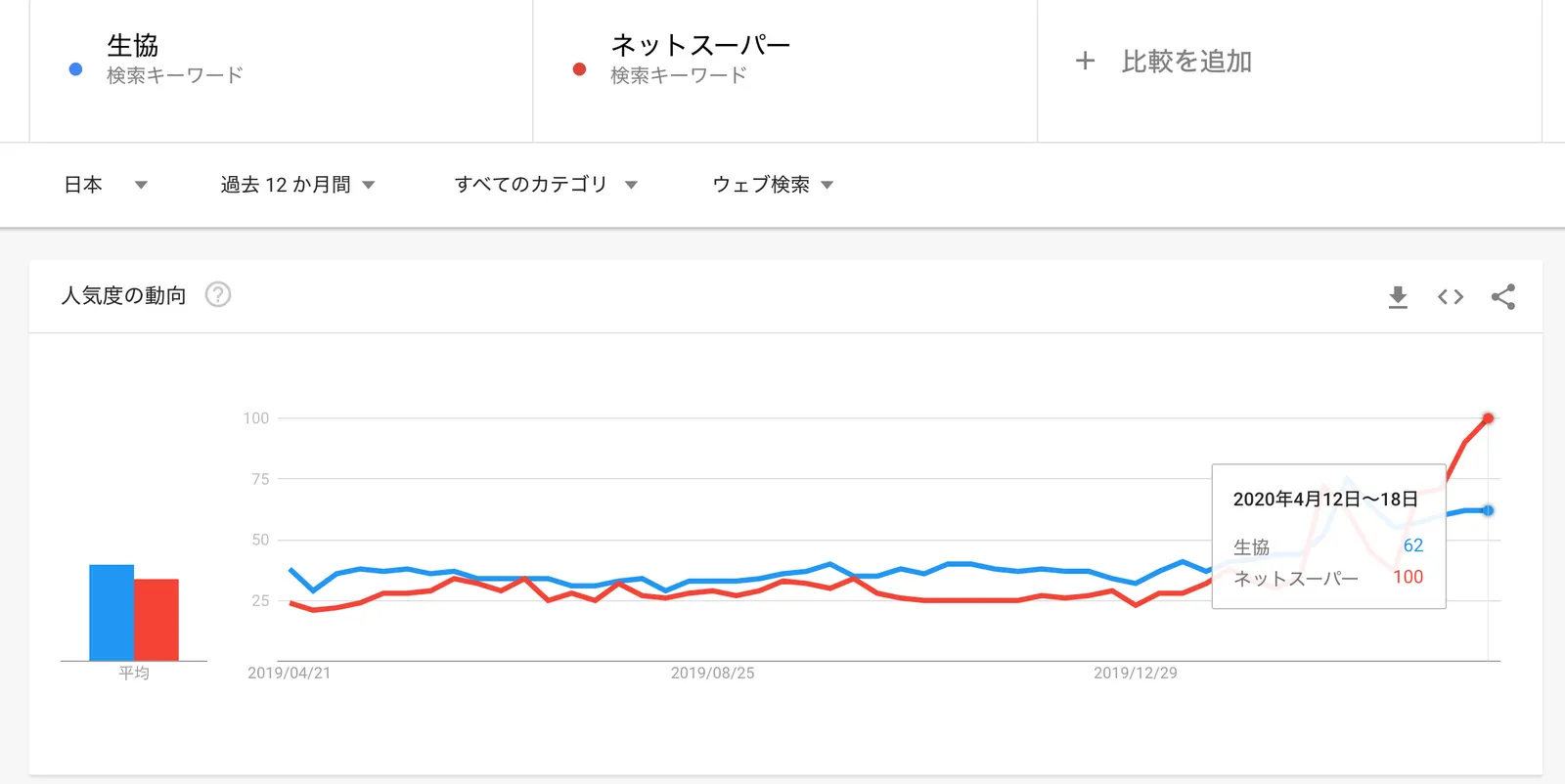

The COVID shock of early 2020 has accelerated this. Google Trends showed, for the first time, online supermarket search volume overtaking co-op search volume — a significant inflection point.

As smartphone-native younger people go through life events like marriage and childbirth and start needing regular grocery delivery, will their first instinct be to reach for a co-op or an online supermarket? When that shift in "top-of-mind" occurs at scale, what kind of digital transformation will co-ops need?

This is something I'm watching closely — both personally and at 10X.

(Postscript: Both co-ops and online supermarkets are currently operating under extreme strain from unprecedented demand spikes caused by COVID. I'm grateful that groceries are arriving at all, and want to express genuine respect for everyone working in this infrastructure under difficult conditions.)

Comments

Share your thoughts or questions. Comments are published after approval.

Write a comment