In April 2021, Grab is going public on NASDAQ via a SPAC merger — the largest of its kind in history. I want to dig into the investor presentation they filed.

When a company goes public through a SPAC (Special Purpose Acquisition Company) merger, no prospectus is required — which typically means many business details are left vague, and projections can be aggressively optimistic. In Grab's case, the acquiring SPAC (AGC) didn't file an S-4, so Grab presented directly to investors. (Thanks to DCM's Hara-san for sharing this.)

SPACs are sometimes seen as "backdoor listings." For example, BAKKT — which also went public via SPAC — was only three years old, recorded its first revenue in 2020, and that revenue was just $28M. Sounds more like a Series A or B startup.

Japan is debating its own version of SPAC, but my personal read aligns closely with Coral Capital's Sawayama-san's series of tweets on this. Worth reading in full.

Grab SPAC Listing Summary

A quick overview of Grab:

- Going public via AGC (Altimeter Growth Corporation, Nasdaq: AGC), managed by Altimeter Capital

- Three-year lockup — AGC is signaling a long-term commitment to post-listing growth

- Valuation: approximately ¥4 trillion — enormous

Here are five takeaways from the presentation. One upfront note: SPAC filings read a lot like VC pitch decks in terms of information quality, content, and density — concise, hitting the key points hard, nothing extraneous. That similarity is interesting in itself.

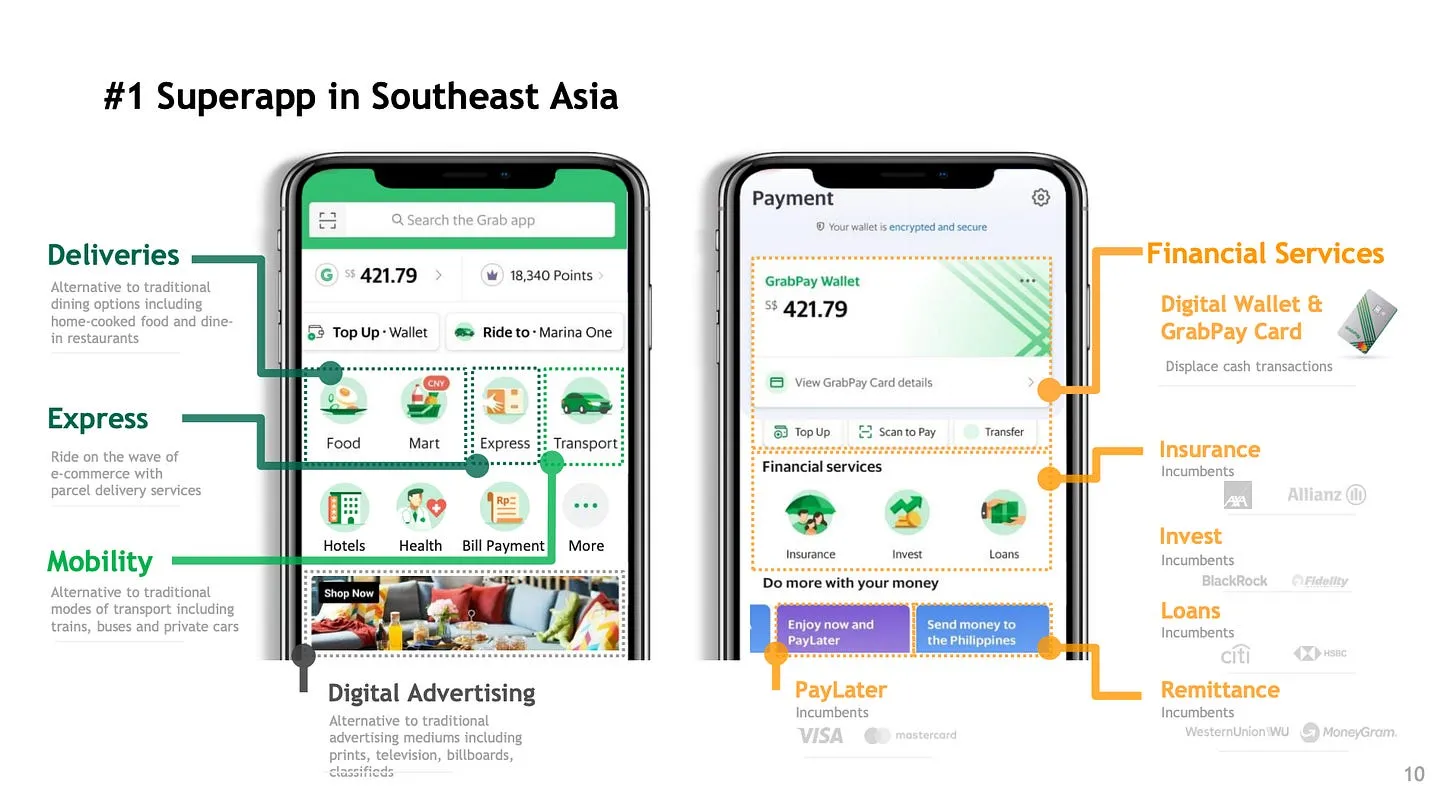

1. Real Superapp

This is Grab's biggest differentiator globally. The following two slides capture it:

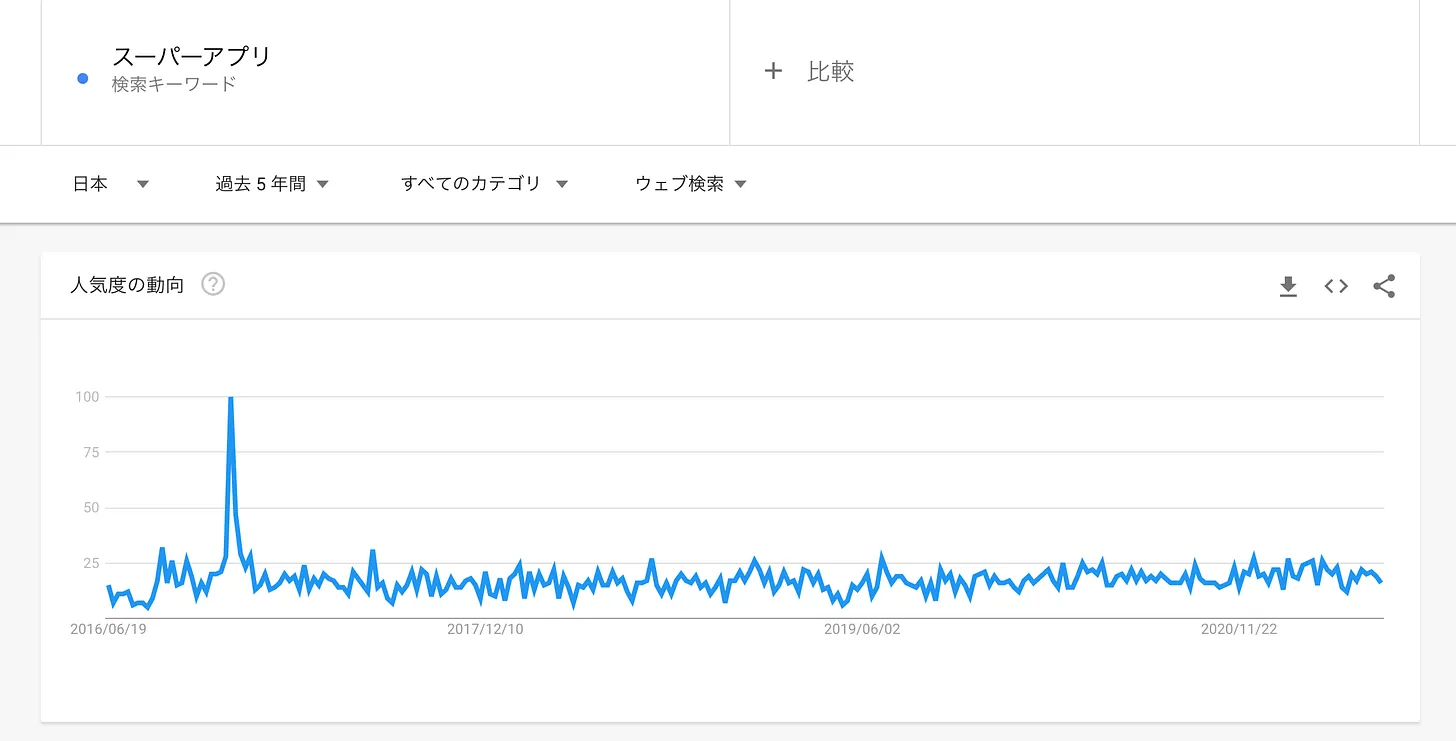

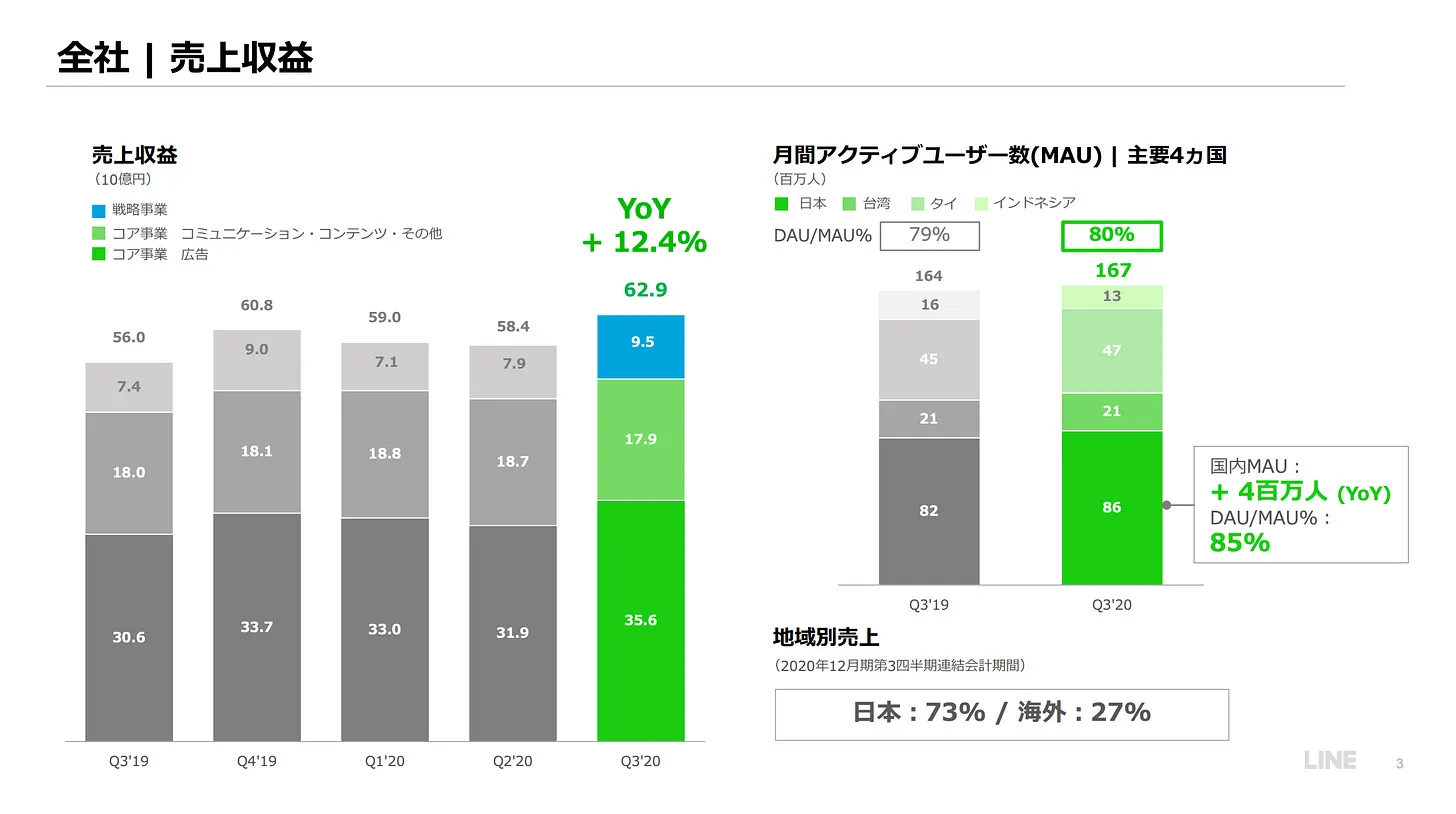

"Super app" was a buzzy keyword in Japan around late 2016, driven by Southeast Asian mobility apps like Grab and Gojek and Chinese giants like WeChat. The buzz faded quickly in Japan. LINE, Yahoo!, and PayPay have all positioned themselves as super app aspirants — but LINE's IR shows that most of its revenue still comes from advertising and content, and for most users it hasn't gone beyond communication plus a bit more.

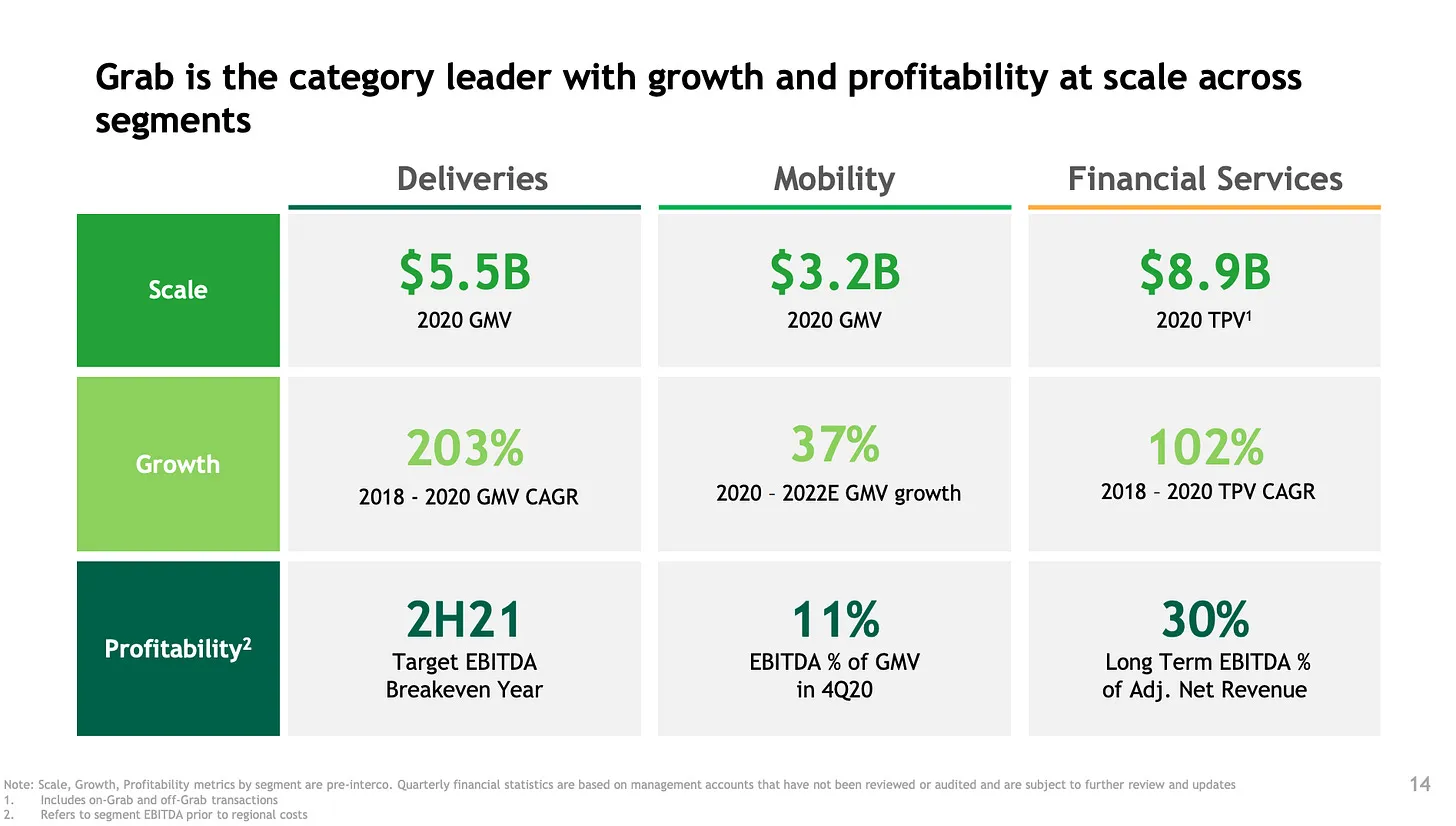

Grab is genuinely realizing the super app vision. Their three service categories each have between ¥300B and ¥900B in GMV:

- Delivery (goods and services)

- Mobility

- Finance (buy-now-pay-later and beyond)

The key mechanism: mobility is the highest-frequency use case, getting users to open the app several times daily. On top of that massive traffic, complex services can be layered effectively.

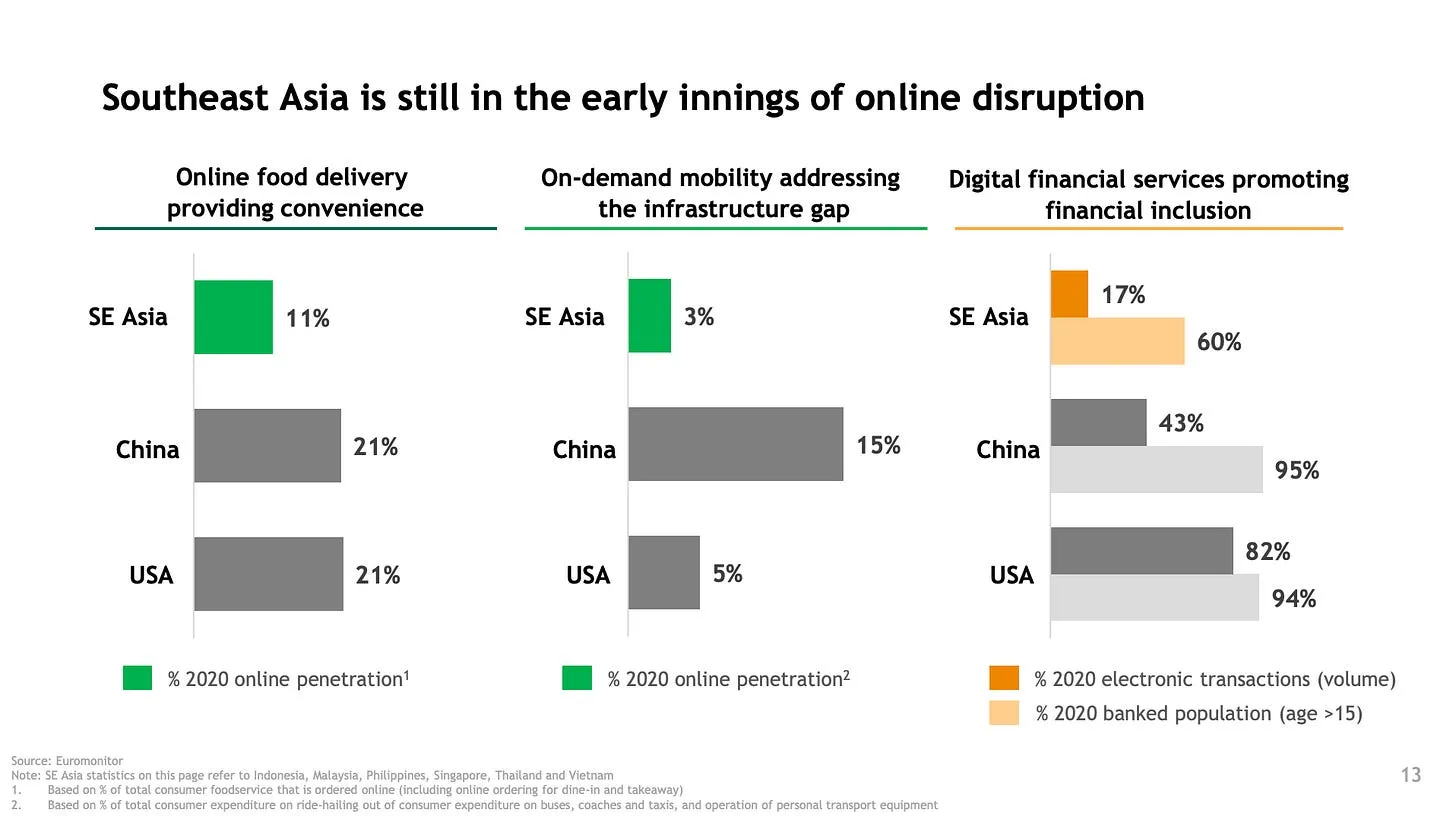

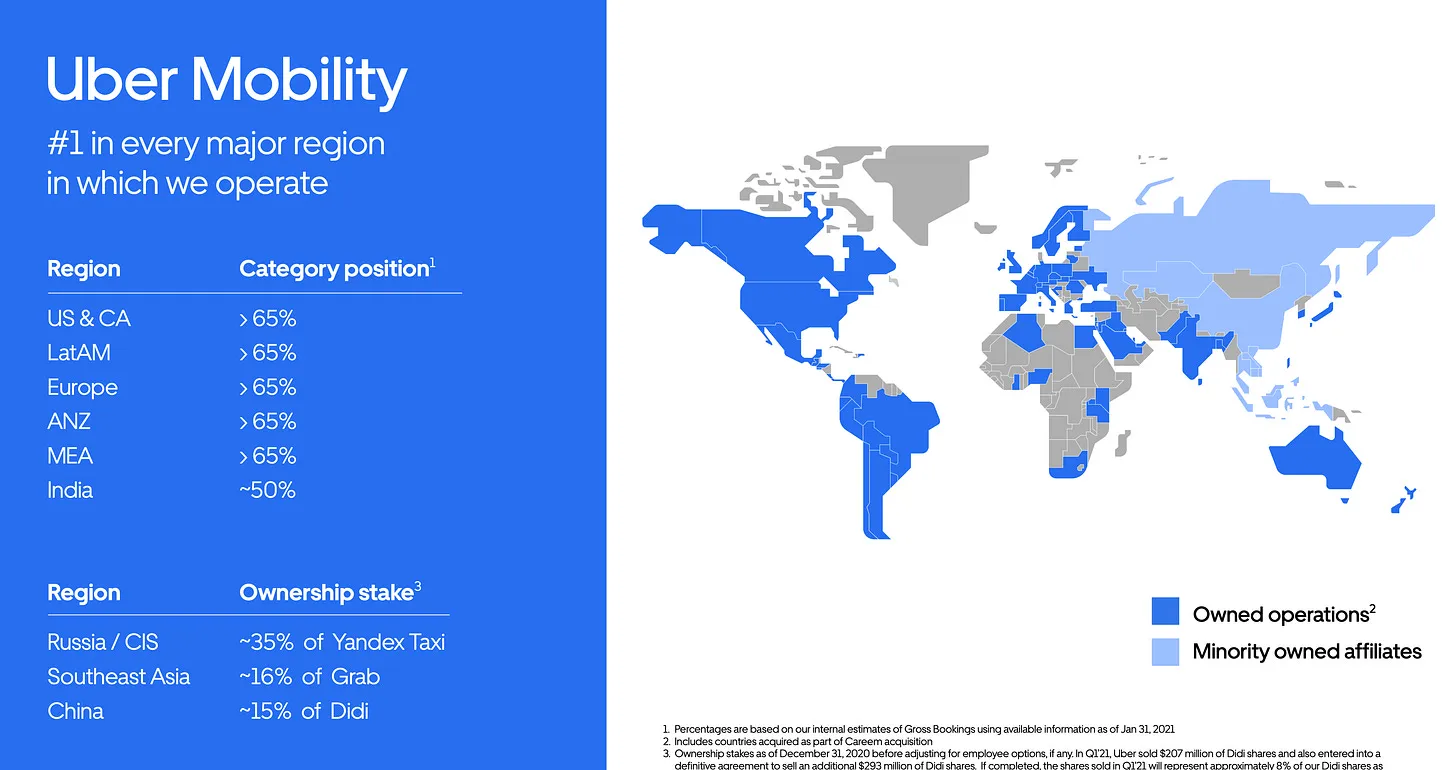

2. Massive Under-Penetrated Market

Despite already handling enormous transaction volumes, Grab's growth story is simple: online penetration in its markets is still very low. They benchmark against China and the US to show how much runway remains.

As someone running a business, this resonates deeply: business growth velocity is more influenced by market growth potential than by any single product or business decision. Investors understand this well — macro is foundational; business and product execution are just the means to catch the wave. This slide is a killer chart that hits that argument cleanly.

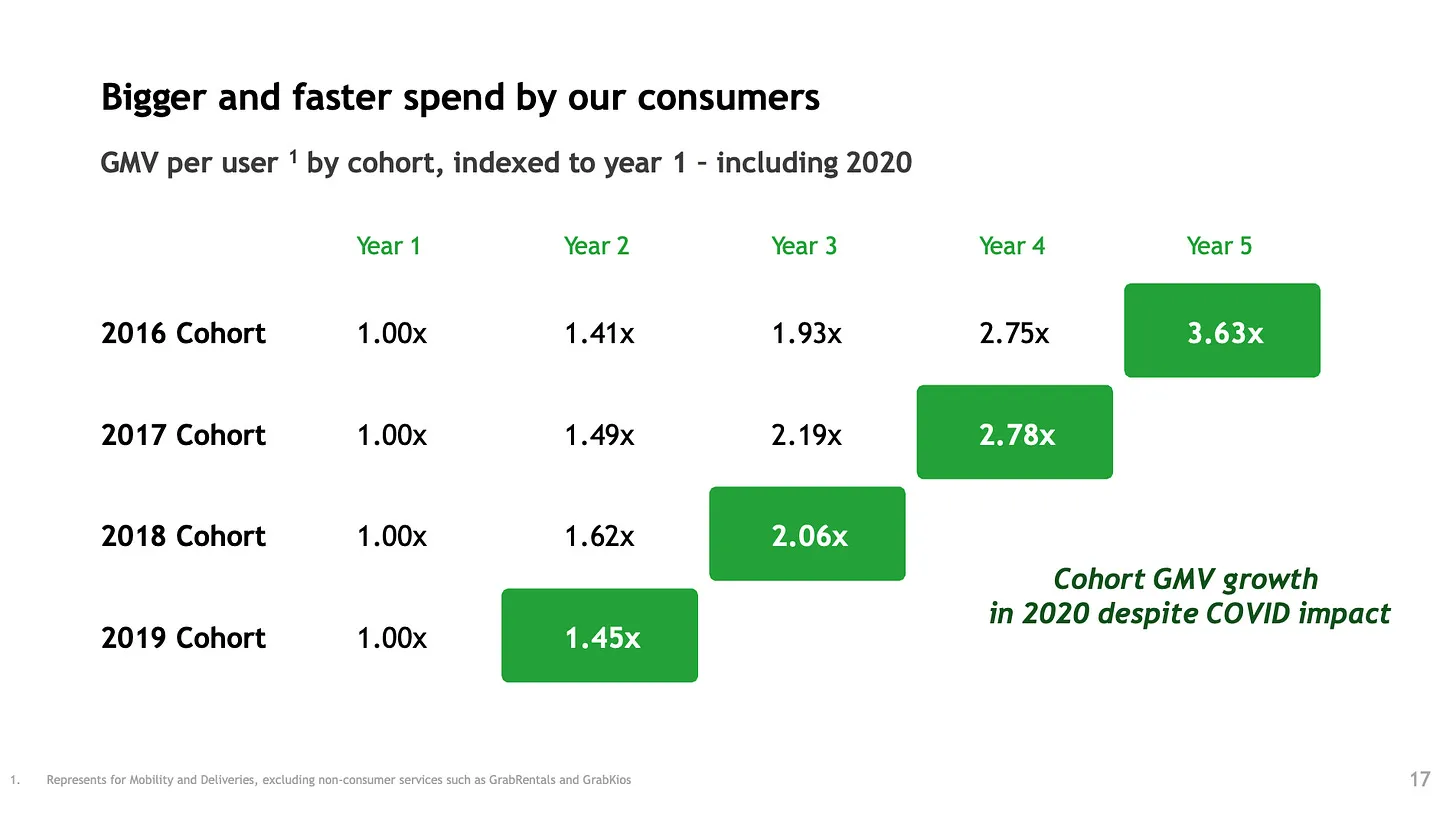

3. Customer PMF

The first slide's dense UI made me think "this looks painful to use" — and I doubt I was alone. Conventional wisdom says mobile apps should be single-use-case to maximize usability.

Grab defies that. The cohort chart below makes the case — it shows abnormally high Net Revenue Retention, unperturbed by COVID. Users spend more and more over time. One chart says it all.

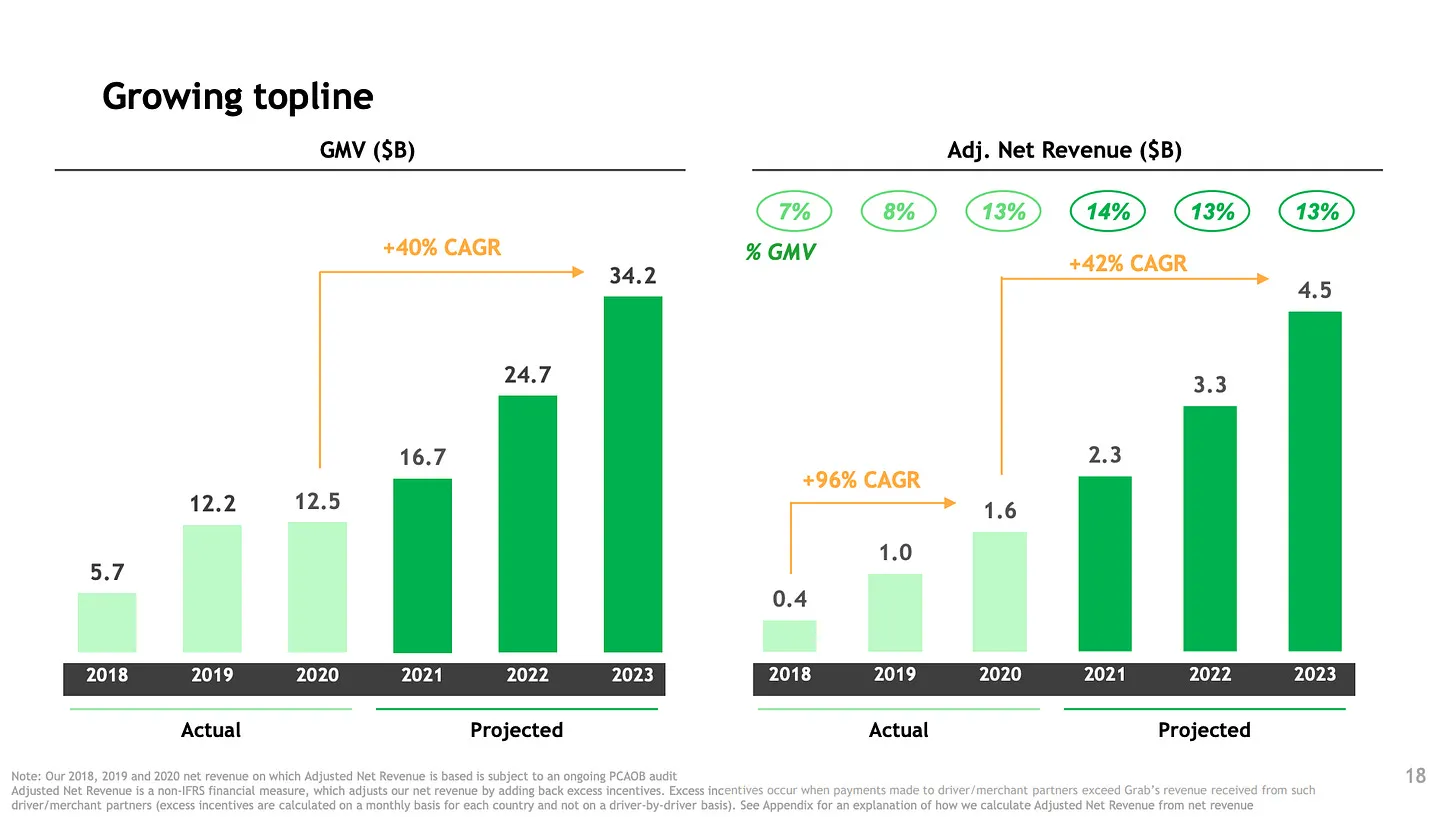

4. Bullish Projections

This is the quintessential SPAC slide. These projections would typically be seen as manipulative in a conventional IPO.

But from the perspective of an unlisted startup pitching to VCs, these look perfectly normal. And combined with the PMF cohort and the penetration story, the growth curve seems demanding but not impossible to believe. SPAC listings may just be the format that lets companies do "startup-style aggressive IR" in the public markets.

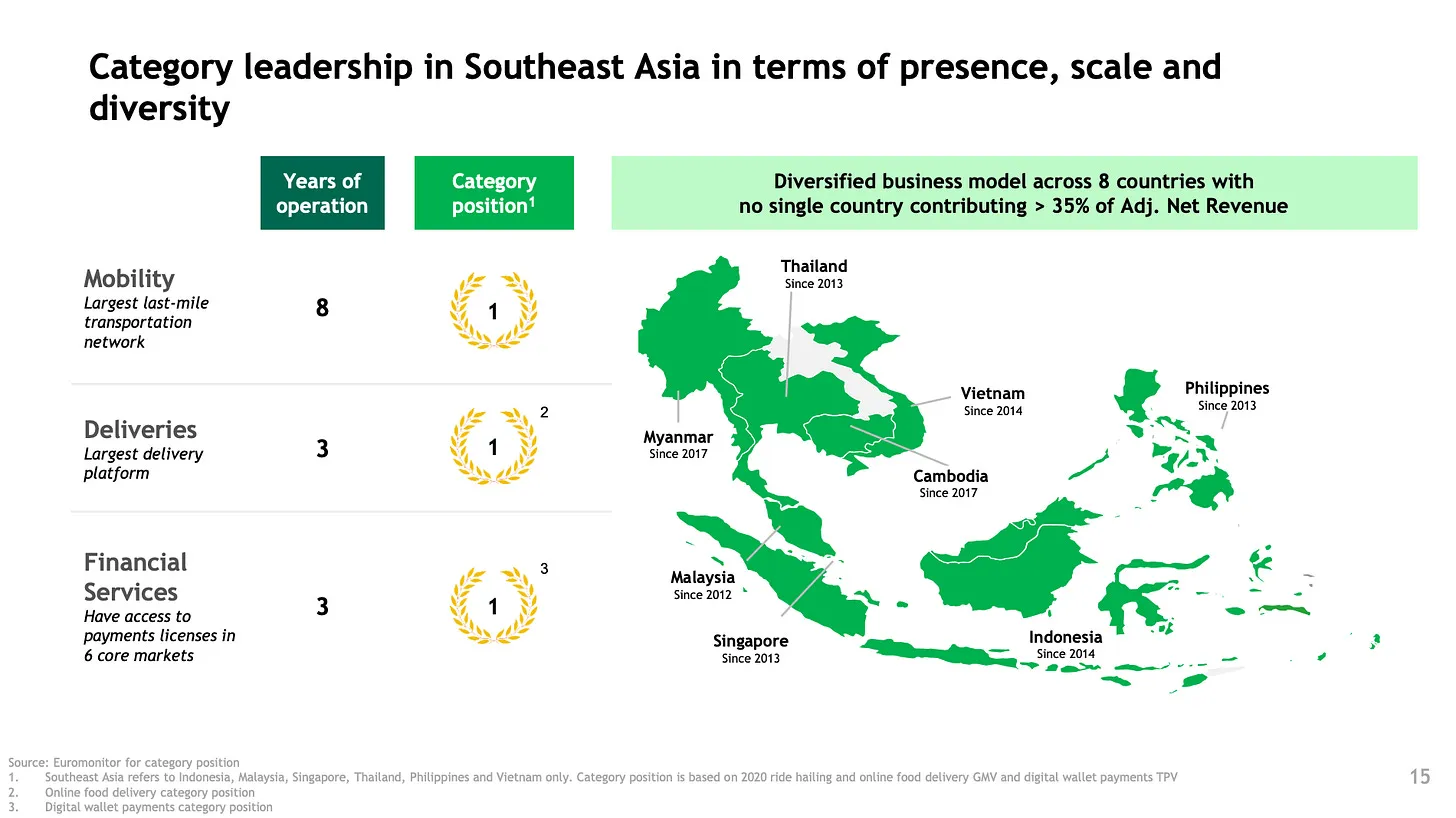

5. Hyper-Local Approach

The final key point: Grab's strategy is unambiguously dominant in Southeast Asia, and nothing else.

The natural comparison is Uber, which explicitly targets the whole world. Serving completely different contexts globally is obviously much harder than serving a region with shared context (even if Southeast Asia has enormous cultural diversity internally).

Grab's focus gives it a cleaner, more believable story for global investors — and it's a strategically honest bet.

Those are the five points I found most valuable. More broadly: anyone working in technology — not just founders — should be reading tech company IR materials regularly. Understanding the rules of the game you're playing is essential. Read them, form opinions, share them.

Comments

Share your thoughts or questions. Comments are published after approval.

Write a comment