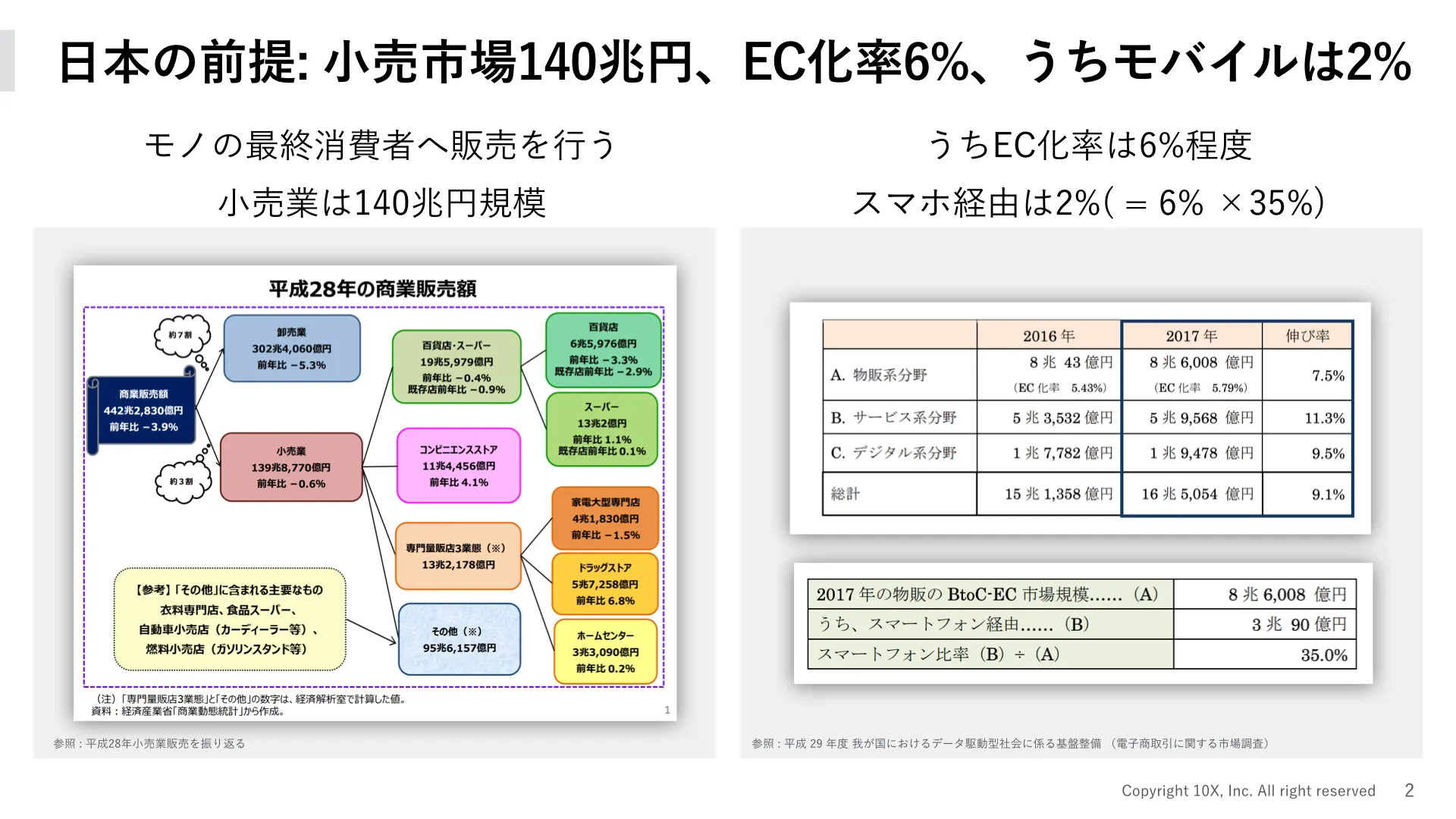

Since launching Tabery and getting deeply involved in food and retail, I've become fascinated by the complexity and depth of the retail industry. Japan's retail market is roughly ¥140 trillion in total value, with online penetration still only around 6% and mobile commerce at around 2%. I want to understand this industry from a product and technology perspective — and eventually help push it forward.

The retail industry, which has historically grown through offline channels, is now seeing two major online trends: OMO (Online Merges with Offline) — integrating online and offline for a seamless experience — and D2C (Direct to Consumer) — using digital product development and customer acquisition to sell directly.

These trends are often discussed in terms of surface-level media narratives: smartphones and social media have fragmented consumer tastes, enabling niche D2C brands to thrive, and so on.

But I suspect there's a deeper gravitational force at work — retail moving toward some form it was always meant to take. What is that force? To understand the present, I want to examine the past: what drove the development of offline retail in Japan, and what were the technological drivers?

The development of retail and its drivers

Retail is a complex business shaped by many forces. The PEST framework (Political, Economic, Social, Technological) is one way to analyze environments — here I'll focus specifically on the technological and product perspective.

One consistent truth about consumer-facing markets: unmet needs drive industry change. Technology has repeatedly played the key role in satisfying needs that previously went unaddressed. The question is: which unmet needs did technology unlock in retail over the past 40 years?

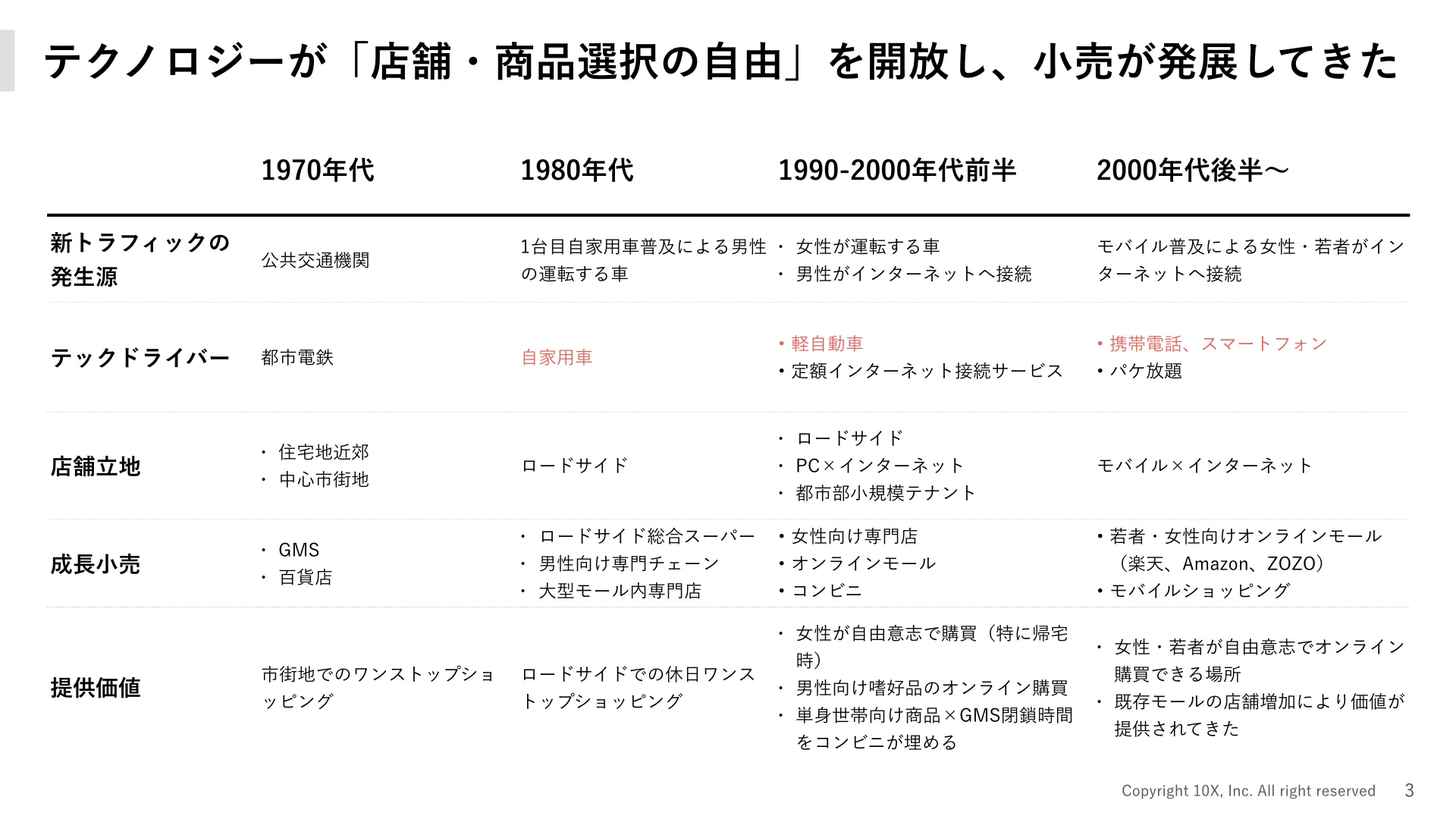

My thesis: the central unmet need was freedom of choice — in stores and in products. In 1970, a typical consumer might have access to just one or two nearby stores. Today, that same consumer can access over 10,000 stores and shop from almost anywhere. The technology and social infrastructure that enabled this transformation drove the entire trajectory of retail.

- The automobile → roads built nationwide to support it

- Mobile phones → radio spectrum opened to enable them

Technology creates the demand, and society reorganizes around it. The result: traffic patterns shifted, and retail winners shifted dramatically with them.

The technologies that most directly unlocked store and product choice were the car and the mobile phone. Among these, the kei car (Japan's compact, affordable light vehicle) and affordable/used smartphones are particularly notable for bringing these technologies to women and younger consumers who hadn't previously had them — creating enormous new traffic.

Era by era

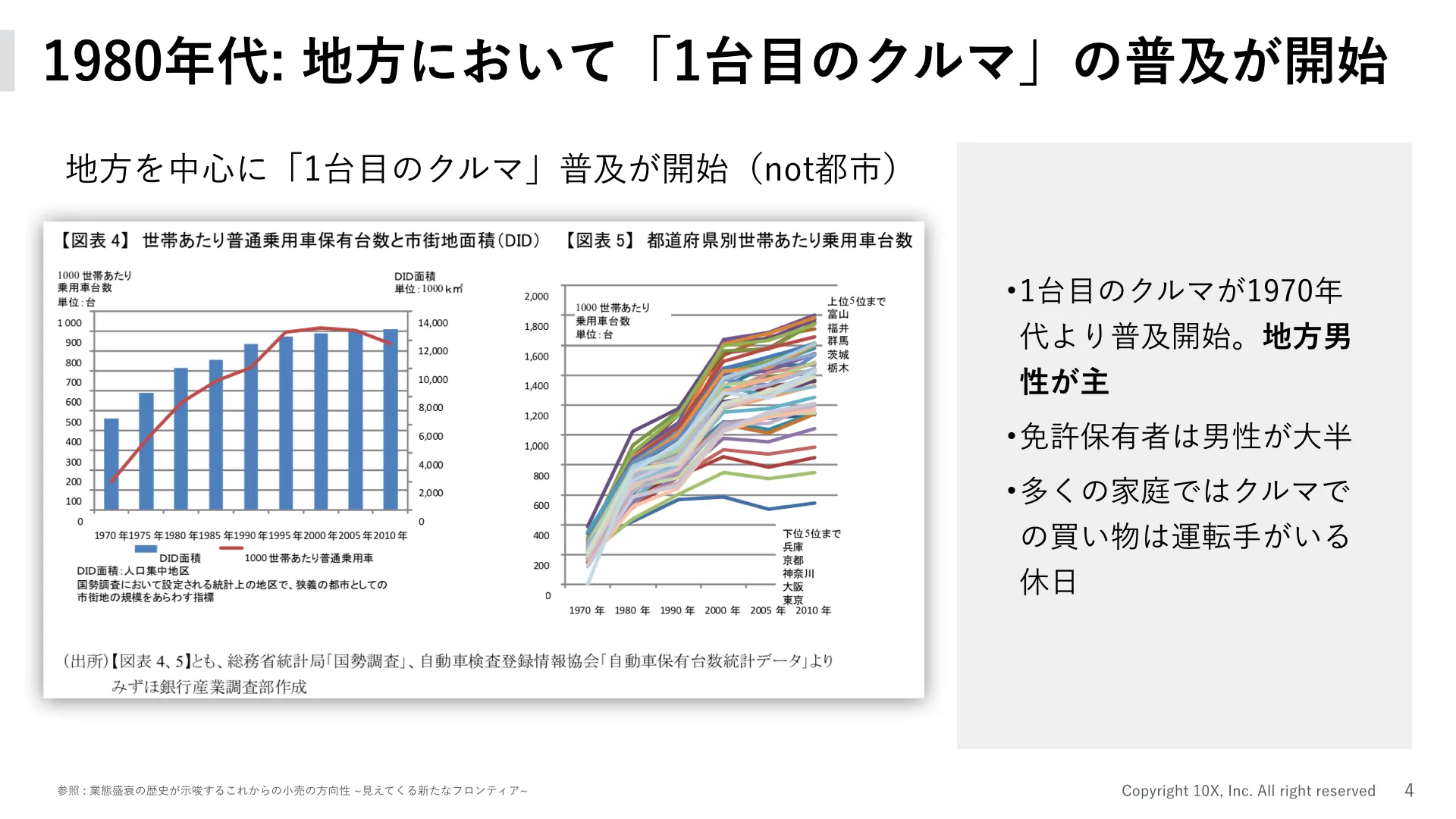

From the postwar period through the 1970s, most consumer movement was on foot or bicycle. As private car ownership expanded, shopping catchment areas evolved:

- Neighborhood shops within walking distance

- Department stores and general supermarkets (JSSS — Japanese Style Super Stores) in urban transit hubs

- Large-format stores on roadside commercial strips (roadside retail)

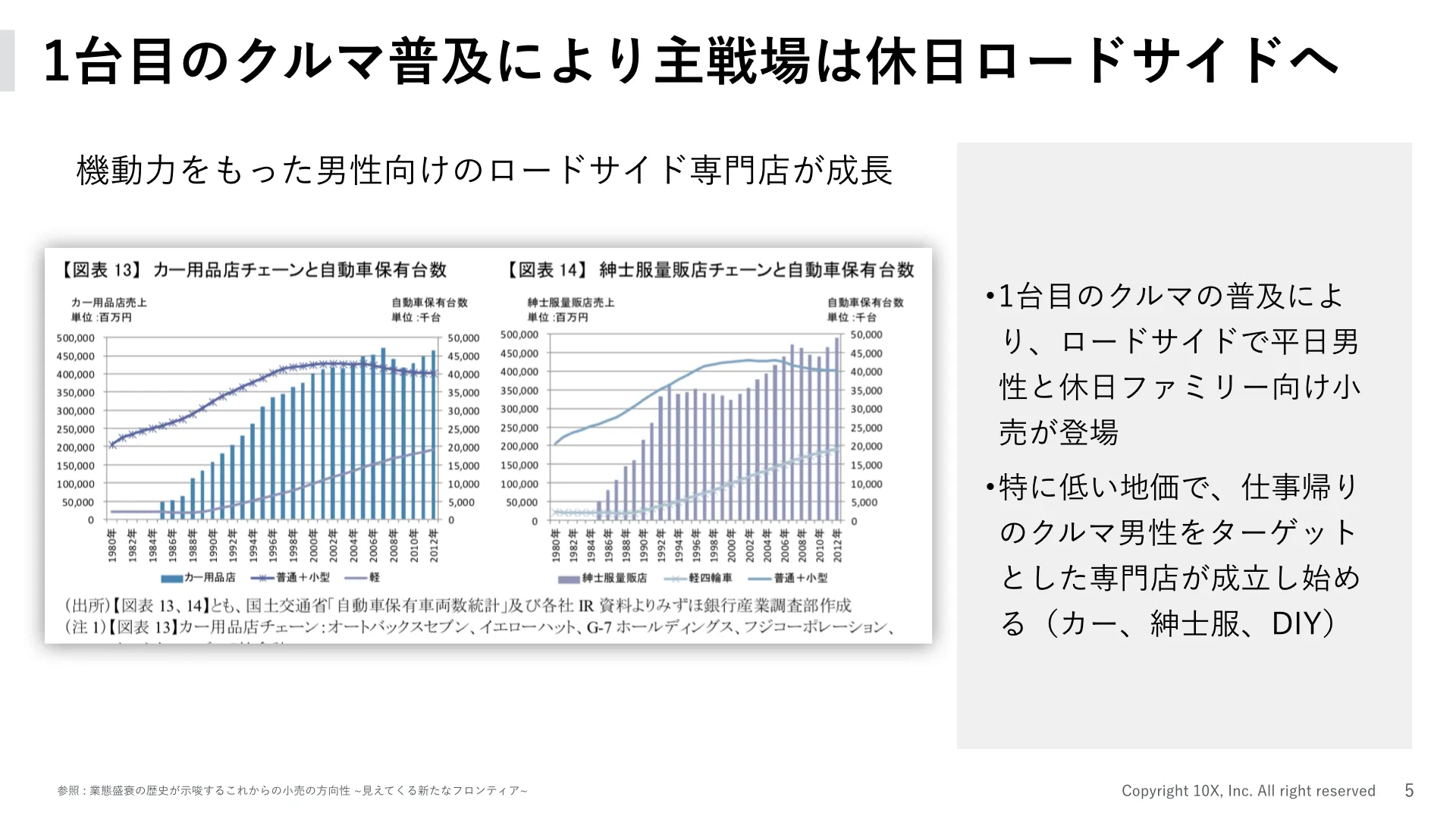

As freedom of store choice expanded, the winning retail format shifted: from urban JSSS, to roadside mall-format general stores, to specialized roadside stores offering better value in specific categories. Men, newly mobile after work, drove the growth of roadside specialty stores in the 1980s: car parts, men's clothing, home improvement centers (home centers).

One fascinating case: in 1980, Seiyu (a JSSS) launched a private label with just 40 SKUs, positioning it as high-quality at a time when Japanese retail was value-driven. It grew through wholesale distribution, then spun out via MBO and became a global brand. That brand is Muji (Ryohin Keikaku). Muji's journey from JSSS category to specialty brand is a direct precursor to what we now call D2C.

Women with mobility as the catalyst

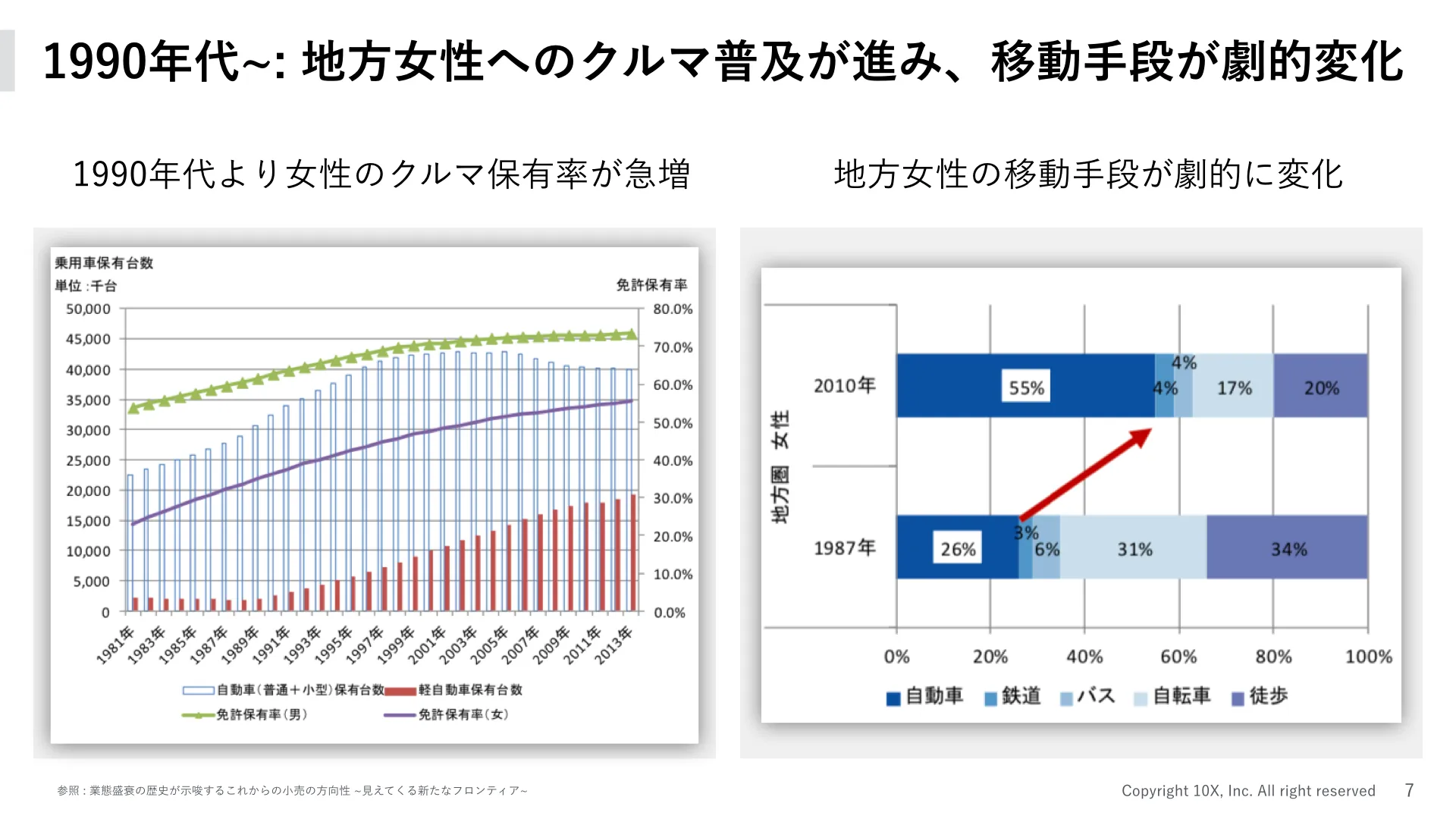

The defining turning point for roadside specialty retail was when women in regional cities began owning their own second household cars — particularly kei cars, which became strongly associated with female drivers.

Kei cars' share of total vehicle ownership rose continuously from the mid-1990s, reaching about half of all cars by 2011. Women's transportation mode in regional areas shifted dramatically: in 1987, 26% traveled by car; by 2010, that figure was 55%.

These newly mobile women, shopping on their own schedules rather than waiting for a weekend family trip, became the engine of demand for female-targeted roadside specialty stores: Uniqlo, Shimamura (a fast-fashion chain), drugstores, and 100-yen shops. These retailers exploded in growth from the late 1990s.

When I first understood the "kei car and Uniqlo" connection, it resonated with my personal experience growing up in a regional area.

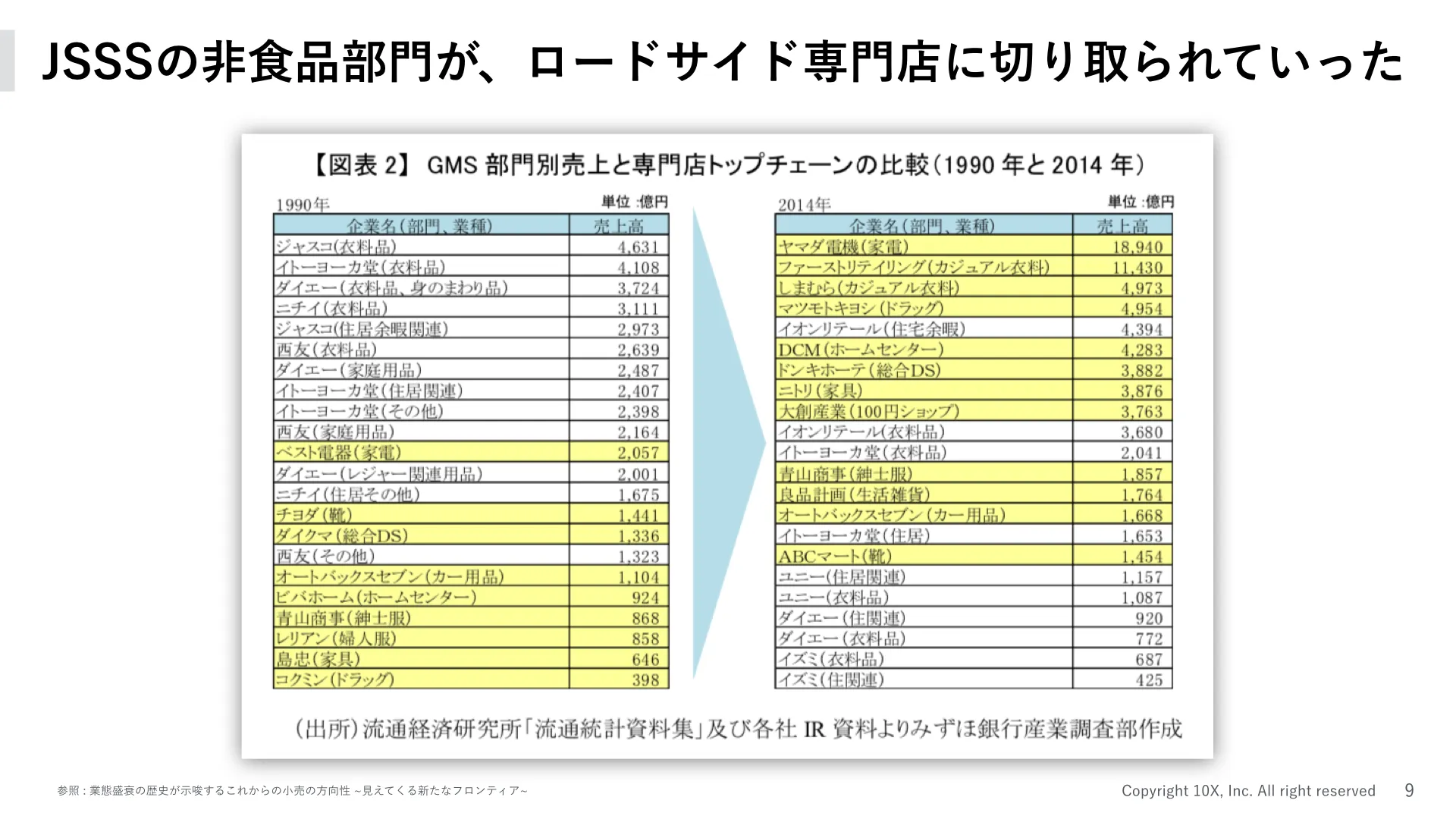

Uniqlo and drugstores sell casual apparel and cosmetics — historically the high-margin items within JSSS. Department stores (like Jusco and Ito-Yokado) had built their model around using food (on the ground floor) to drive traffic, then capturing profit from apparel and cosmetics (on upper floors). The model depended on how many customers who came for groceries would walk through clothing and cosmetics.

When women gained freedom of store choice and began seeking better value and more tailored experiences, JSSS — vast, inconvenient for targeted shopping — could no longer keep up. Their business model was dealt a blow they never fully recovered from.

Freedom of movement drove retail on cheap roadside land

To summarize:

- 1970s: Department stores and JSSS thrived in urban transit hubs

- 1980s: Roadside JSSS and men's specialty stores followed car ownership

- Late 1990s–2000s: Roadside women's specialty stores exploded as female mobility spread

As technology unlocked choice, the location and category of winning retail shifted: to cheaper land, more specialized products.

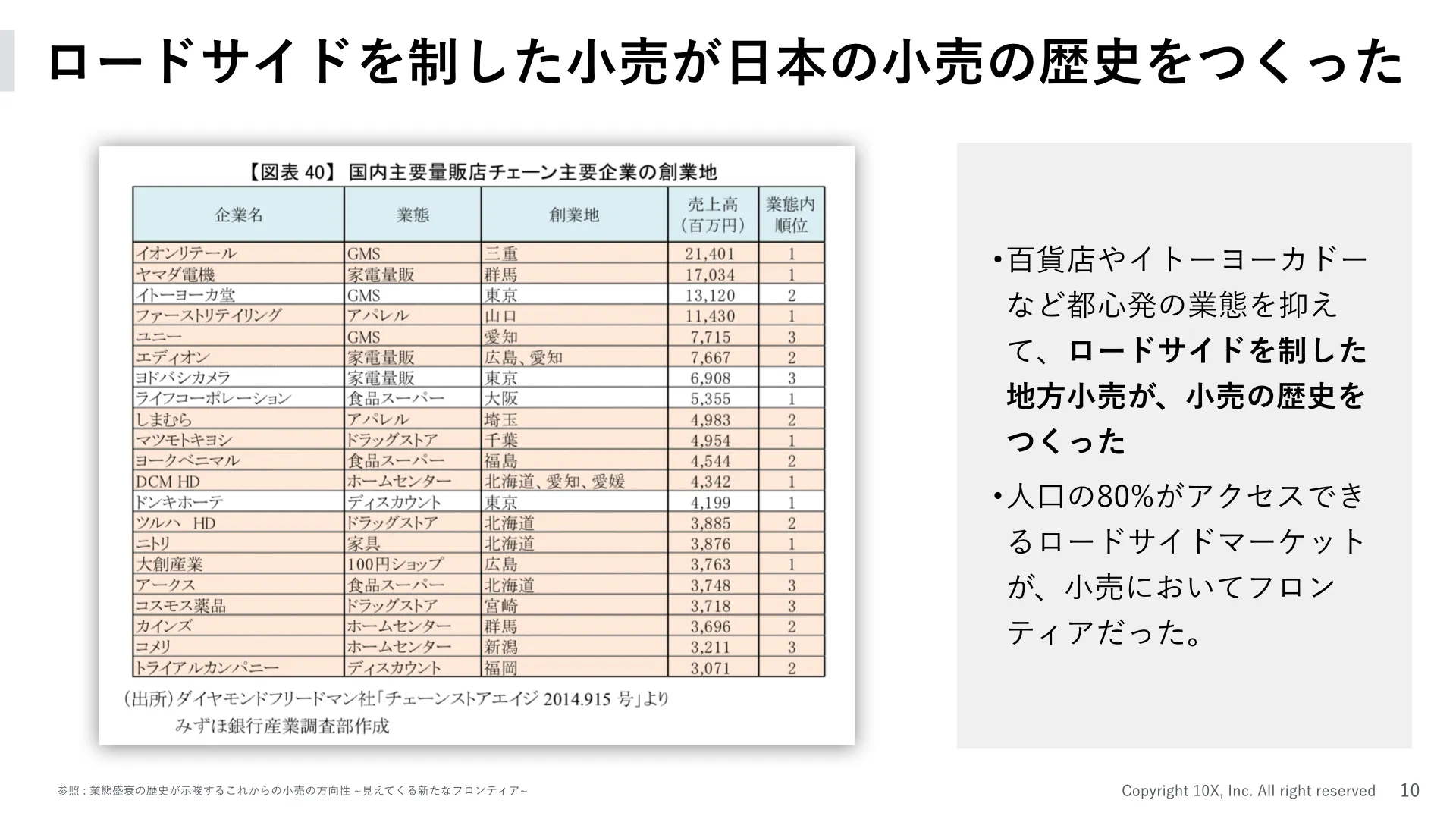

The answer for location turned out to be roadside strips — accessible to 80% of the population via arterial roads, with dramatically cheaper land and available parking. Almost all the major retail chains that now dominate Japan were founded in regional areas, not Tokyo or Osaka. The retailers who won the roadside wars made Japanese retail.

These roadside winners then used their cash to pursue three simultaneous strategies: SPA (vertically integrated manufacturing-retail), international expansion, and online expansion.

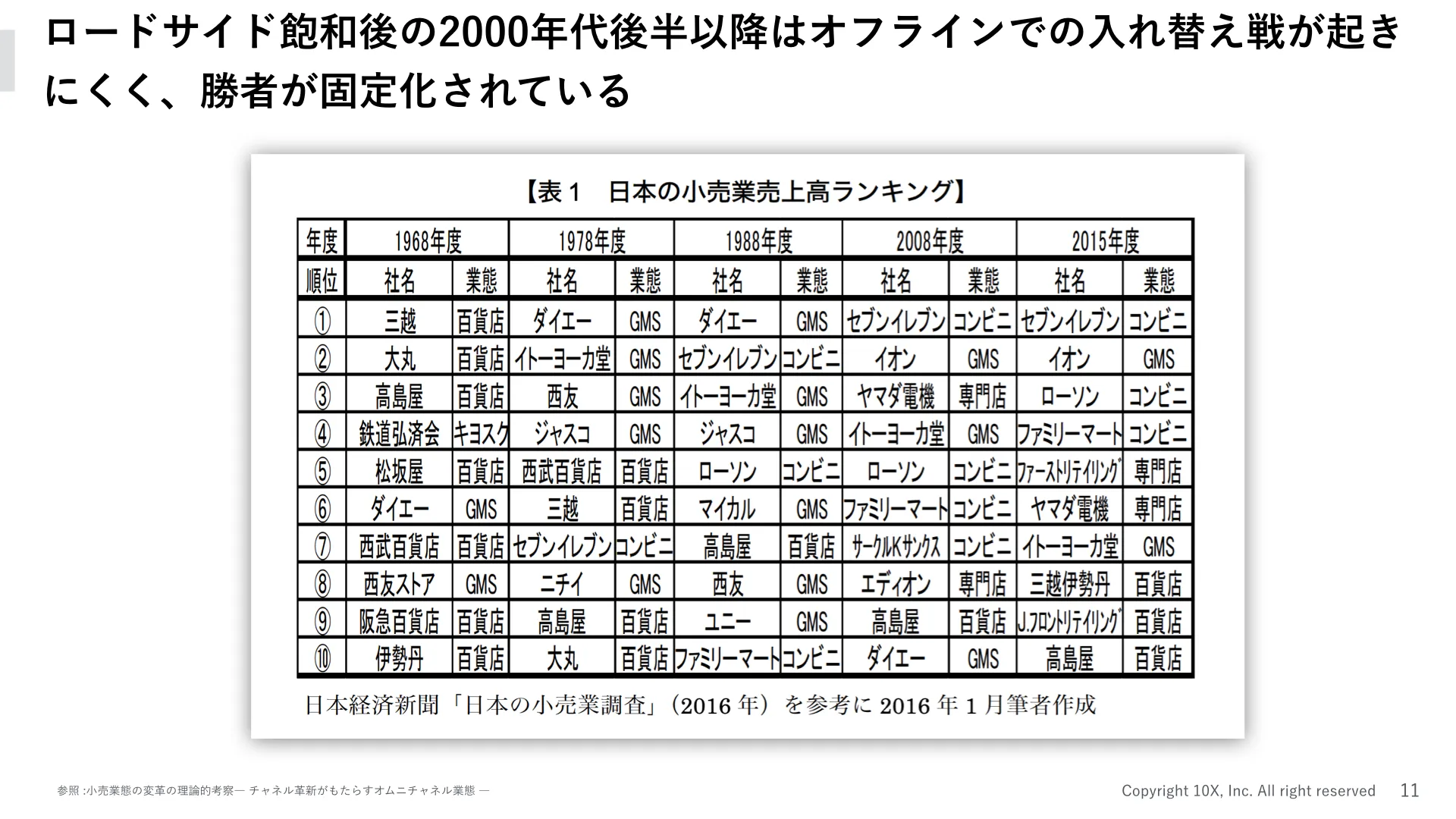

But roadside has been saturated for about a decade. Traffic patterns haven't changed significantly. The roster of winners has barely shifted. Entry and disruption have become much harder.

The core driver of offline retail growth was freedom of store and product choice, enabled by the spread of the automobile. The saturation of roadside with the completion of car ownership has left offline retail in stagnation for the past decade.

Convenience stores: the exception that proves the rule

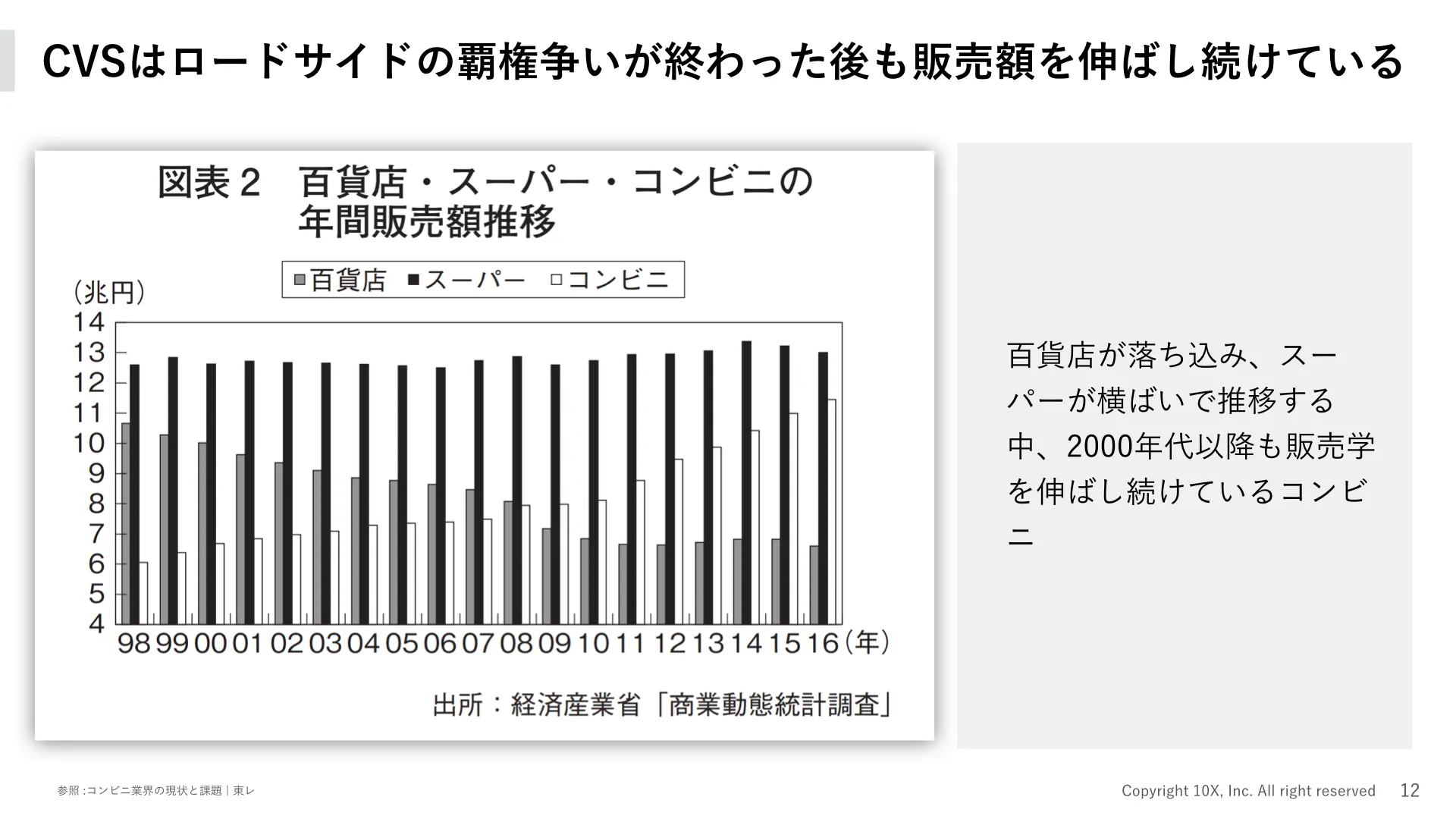

There's one major retail category that grew through a different logic: convenience stores (CVS in Japan, like 7-Eleven, Lawson, and FamilyMart — all ubiquitous nationwide).

CVS continued growing in transaction volume even as roadside saturated — reaching ¥12 trillion annually. This requires a different explanation.

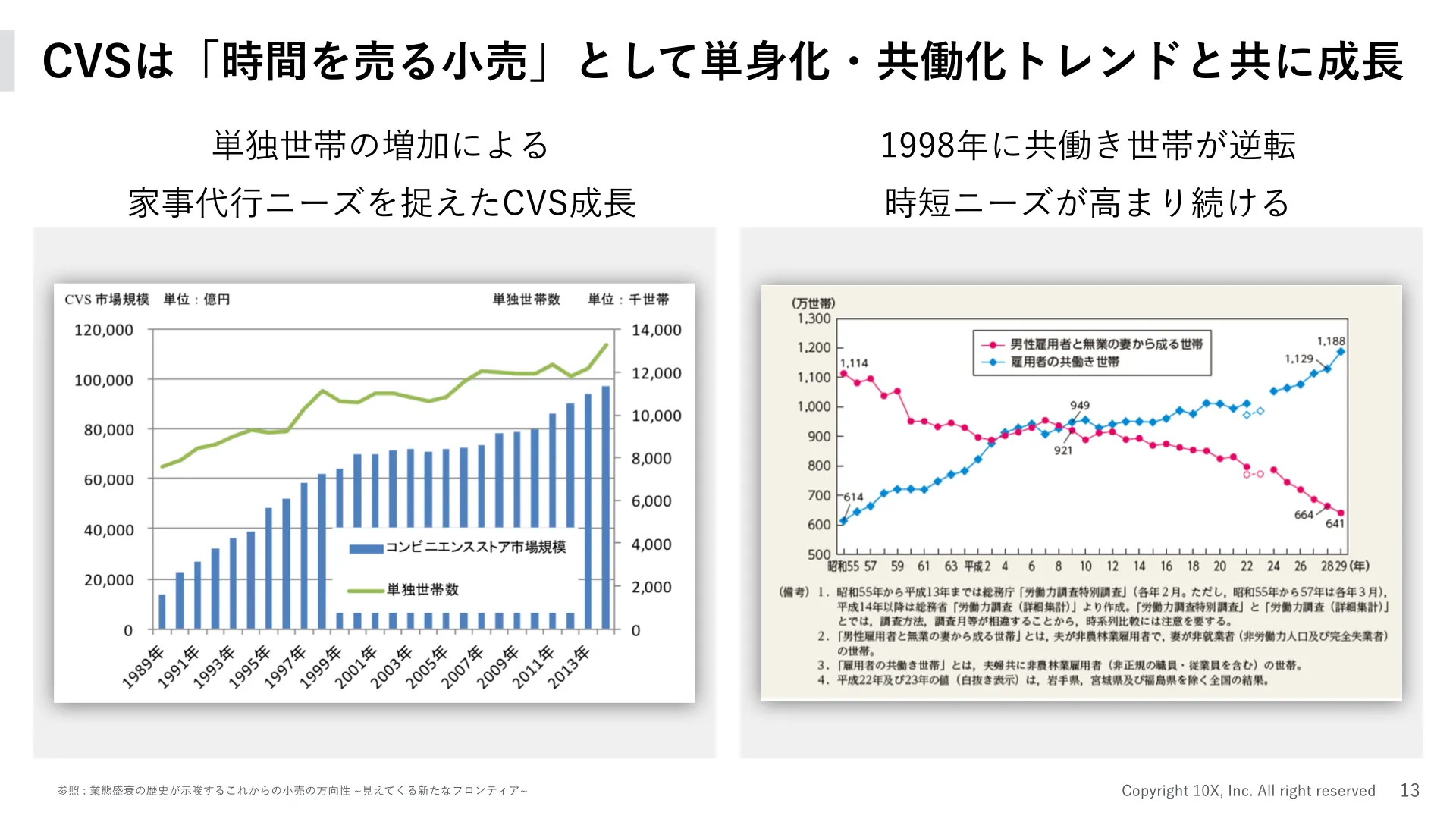

While other retailers adapted to technology-driven changes in movement patterns, CVS growth was driven by social change — specifically, the rise of single-person households and dual-income households. These created demand for time-saving household services, and CVS stepped in to fill them.

A ¥140 bottle of water that costs ¥88 at a supermarket, a ¥120 rice ball that you could make at home for ¥50 — the premium is for time. CVS sells time.

Japan's first 7-Eleven opened in Toyosu in 1974. It started as a niche service — capturing demand when other stores were closed, serving busy people making small urgent purchases. But it grew via franchise and density strategy (dominating specific neighborhoods), and kept expanding its service offering: proprietary products, parcel delivery, bill payment, government services, concert tickets. Today it's almost easier to list what you can't do at a convenience store.

As a result, CVS evolved from a simple time-saver into something resembling the "one-stop shopping" value that JSSS once provided — but in a much more convenient, high-quality form.

The late-2010s growth retailers — major drugstores and Don Quijote (a discount-variety chain with a cult following) — tell the same story. The winning retail format in the saturation era is the composite experience: multiple categories and services under one roof.

Summary

Retail has many variables, and many technologies have been invented within it. But if I had to name the single most important variable for retail growth, it's Where — location and timing.

In offline retail, the only technology that moved "Where" was the car.

The completion of car ownership and the saturation of roadside began offline retail's decade-long stagnation. In the 2010s, the battleground shifted to online.

The history of online retail closely mirrors the offline story. And the current trends of OMO and D2C can largely be understood through the lens of the "late roadside to saturation" period. Convenience stores and drugstores offer useful hints about what comes next. I'll explore that in the next post.

Comments

Share your thoughts or questions. Comments are published after approval.

Write a comment